[ad_1]

The excellent news: Client Worth Index (CPI) got here in modest at 0.4%, with a year-over-year 4 deal with at 4.9%. I anticipate this can proceed to fall over the following few months and is more likely to have a 3 deal with earlier than Christmas, perhaps even Halloween.

The inflation that appeared so pernicious in 2021 and into 2022 was pushed by the mixture of three issues:

– Distinctive pandemic elements

– Large financial stimulus (CARES ACT I, II & III)

– Structural (long-term) shortages in labor and single-family houses

The distinctive setting of the COVID-19 lockdown for 18 months and the pent-up calls for that adopted its finish don’t have any comparables in historical past. No the present type of inflation is nothing just like the Nineteen Seventies, neither is it just like what occurred within the mid-2000s.

This has been a novel and (dare I say it) unprecedented set of things which have despatched costs increased regardless of the intentions of the Federal authorities and the FOMC.

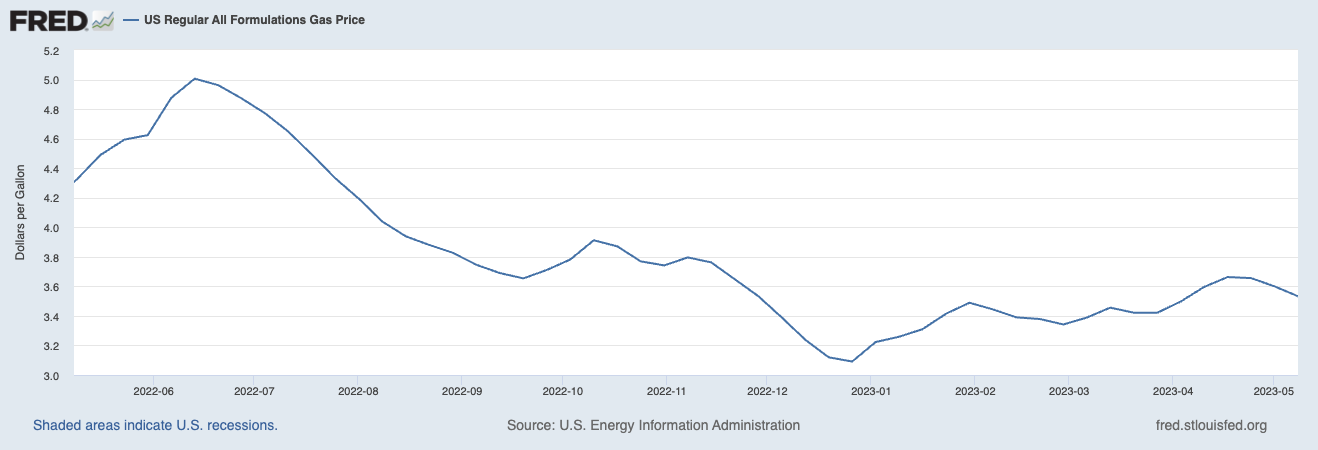

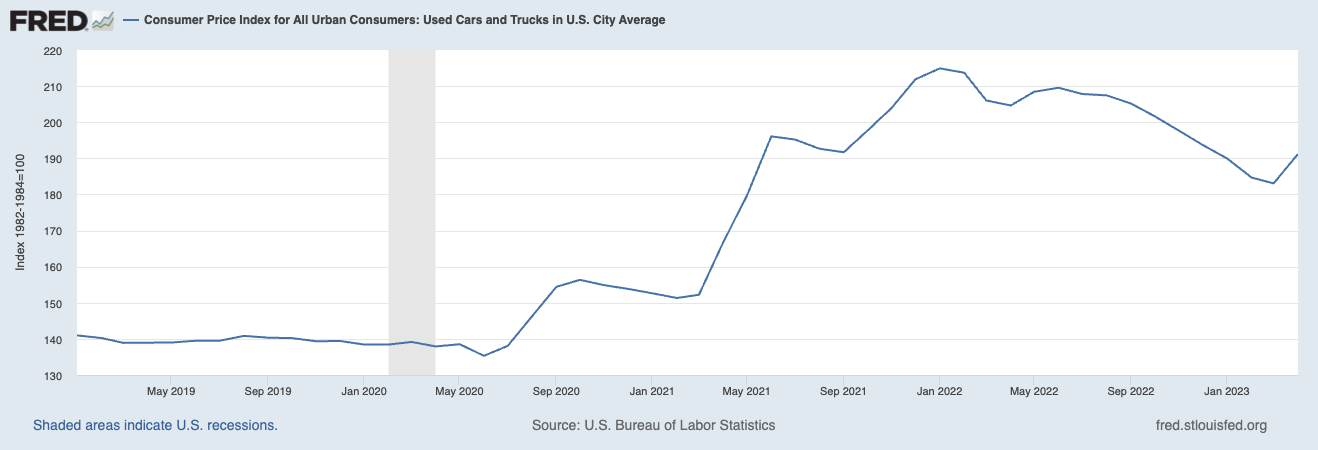

However CPI knowledge is all the time lagging and backward-looking: Think about the large risers in April have been shelter, used automobiles and vans, and gasoline.

Gasoline costs in April are far behind the curve, as oil costs fell under $70 this week. You possibly can see the general pattern in gasoline is decrease, with some volatility because the summer time driving season approaches.

The identical is true for Used Automobiles and Vans, they’re nonetheless elevated because of the scarcity of latest automobiles which traces itself to the slowly easing provide shortages of semiconductors. However increased charges are sending them in the correct route.

Final, Shelter: It’s being pushed increased by the Fed itself, as they’ve despatched mortgage charges a lot increased thereby making rental charges increased.

The outdated regime of a 2% inflation goal is useless. I might transfer the goalposts in direction of a extra rational 3% over the following 12 months. To get again to 2% inflation goal, the financial system would want some mixture of ZIRP, or increased unemployment, or greater than a gentle recession.

The Fed’s new motto needs to be 3% or bust…

Beforehand:

For Decrease Inflation, Cease Elevating Charges (January 18, 2023)

Press Pause (Might 3, 2023)

Transitory Is Taking Longer than Anticipated (February 10, 2022)

Who Is to Blame for Inflation, 1-15 (June 28, 2022)

How the Fed Causes (Mannequin) Inflation (October 25, 2022)

[ad_2]

Source link

{kind=link}