[ad_1]

The worldwide workplace funding sector, much like different sorts of actual property, is coming beneath some stress from the macro-economic setting. Nevertheless, sturdy fundamentals ought to preserve funding yields largely steady in lots of key markets, together with Paris, London, Sydney, Mumbai and Dubai, Savills says in its first International Capital Markets Quarterly replace.

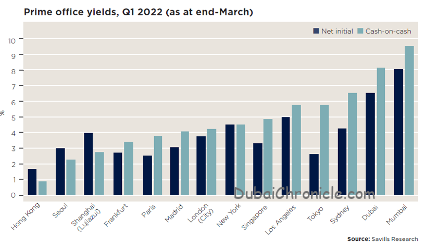

Edward Value, Affiliate Director – Capital Markets Center East at Savills mentioned: “Leasing exercise throughout the workplace market in Dubai has remained sturdy during the last six months. The variety of enquiries have steadily elevated and town has benefitted from the provision of Grade An area at inexpensive value in comparison with different workplace hubs throughout EMEA. The workplace market in Dubai stays a beautiful funding alternative with estimated cash-on-cash prime workplace yields over 8%, second solely to Mumbai and highest among the many western and Asian international locations ranked.”

Savills has assessed the seemingly interaction between the top-down (inflation, rate of interest rises, geopolitical uncertainty) and bottom-up elements (restricted availability of inventory and weight of cash inflicting competitors between traders) that can decide the pricing of workplace property over the subsequent 12 months in main international cities.

The US could also be most uncovered to macro top-down elements, with expectations of a big tightening in monetary circumstances and restricted pricing energy for landlords probably resulting in yields rising in New York and Los Angeles. European traders in the meantime could proceed to learn from strong occupier demand and a scarcity of provide within the prime and core segments of the market, holding yields steady.

In the meantime, in Asia, home market-specific traits dominate the regional narrative. In Tokyo for instance, cash-on-cash returns will stay enticing given little upward stress on rates of interest, which is able to assist additional yield compression, whereas the outlook for Shanghai has deteriorated amid a difficult home financial backdrop.

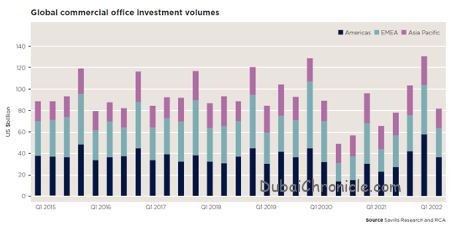

The restoration in occupier demand and a scarcity of prime workplace inventory throughout most main markets has inspired higher investor exercise. International funding in places of work hit a report of US$130 billion within the closing quarter of 2021, with momentum spilling into the start of this 12 months. The US$82 billion transacted globally in Q1 was up 25% on the 12 months, and solely 3.5% shy of the five-year common main as much as Covid-19.

Elevated uncertainty will underpin a flight to security which, mixed with an rising deal with ESG, will favour Grade A workplace buildings in main cities.

[ad_2]

Source link

:max_bytes(150000):strip_icc()/Health-GettyImages-1477523726-d9489f5e044241b097588b0636bf7561.jpg "Solar Poisoning: Indicators and Signs")

{kind=link}