[ad_1]

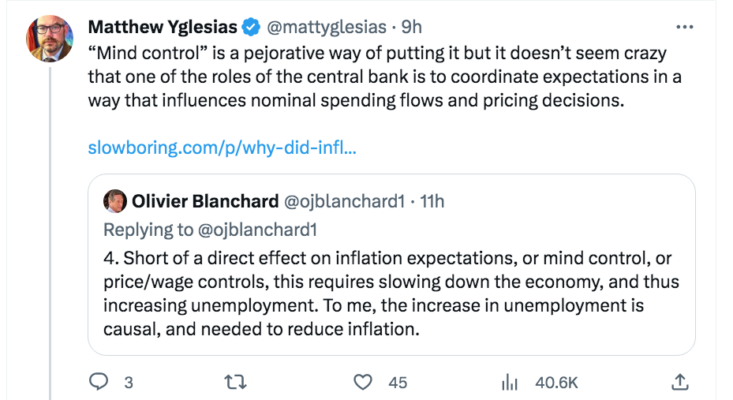

In latest days, there’s been a twitter debate about whether or not adjustments in employment drive the inflation course of:

I considered this debate when studying in regards to the sudden rise within the Argentine worth degree. Right here’s Bloomberg:

At outlets all throughout Argentina, from cafes to kitchenware distributors, scores of small-business house owners awakened Monday to search out some model of the identical discover of their inboxes: Their suppliers had hiked costs 20% in a single day. . . . Sharp worth hikes appeared early for electronics and residential home equipment Monday. MacStation, an official reseller of imported Apple merchandise in Argentina, raised its pc costs practically 25% whereas native e-commerce web site Precialo, which tracks pricing historical past, confirmed fridge, washer and TV worth tags north of 20% previously week.

In equity to Blanchard, costs are extra versatile in a excessive inflation nation similar to Argentina. However these types of nations symbolize a form of lab experiment: What occurs while you quickly enhance the foreign money inventory in a rustic not on the zero sure? Or (on this case): What occurs when a political shock happens that results in sooner anticipated future progress within the cash inventory? The result’s an nearly rapid improve within the worth degree. Yglesias is appropriate. It’s not “thoughts management”; it really works by way of the general public having a rational forecast of the long run path of coverage. Argentine residents have been right here earlier than.

I don’t have knowledge on the Argentine labor market, however I doubt that the unemployment charge fell sharply final evening. The Phillips curve doesn’t inform us something helpful in regards to the inflation course of in Argentina.

In truth, it’s financial coverage that drives inflation–not the labor market. In an economic system the place costs aren’t sticky, it does so with out a lot change in unemployment. In an economic system with sticky costs, unemployment usually adjustments as inflation adjustments. However that’s an impact, not a trigger.

In America, inflation is far decrease and costs are stickier. However even right here, adjustments in financial coverage have an effect on nominal GDP progress in a really quick time period, inside weeks. The so-called lengthy and variable lags are a fable. Economists have used lags as an excuse for the truth that they use the unsuitable mannequin. Keynesians use rates of interest to point the stance of financial coverage, whereas monetarists depend on the financial aggregates. Each of those indicators are flawed. When their predictions don’t pan out, they use lengthy and variable lags as an excuse.

If I have been making an attempt to make a dwelling as a fortune-teller, I’d say, “After an extended and variable time period, I see you having some well being issues.” Within the Sixties, it took 10 years for rising rates of interest to provide a recession. The rate of interest improve of 1994 didn’t result in recession till 2001.

The most effective indicator of financial coverage is market forecasts of future NGDP. And financial coverage impacts market expectations of future NGDP with no lag in any respect. When subsequent 12 months’s anticipated NGDP declines, present NGDP tends to fall after a comparatively quick time period. There are not any lengthy and variable lags in financial coverage.

Replace: Kevin Erdmann factors out that our worth degree would possibly quickly be a bit much less sticky.

[ad_2]

Source link

:max_bytes(150000):strip_icc()/Health-GettyImages-1477523726-d9489f5e044241b097588b0636bf7561.jpg "Solar Poisoning: Indicators and Signs")

{kind=link}