[ad_1]

The next tweet caught my eye:

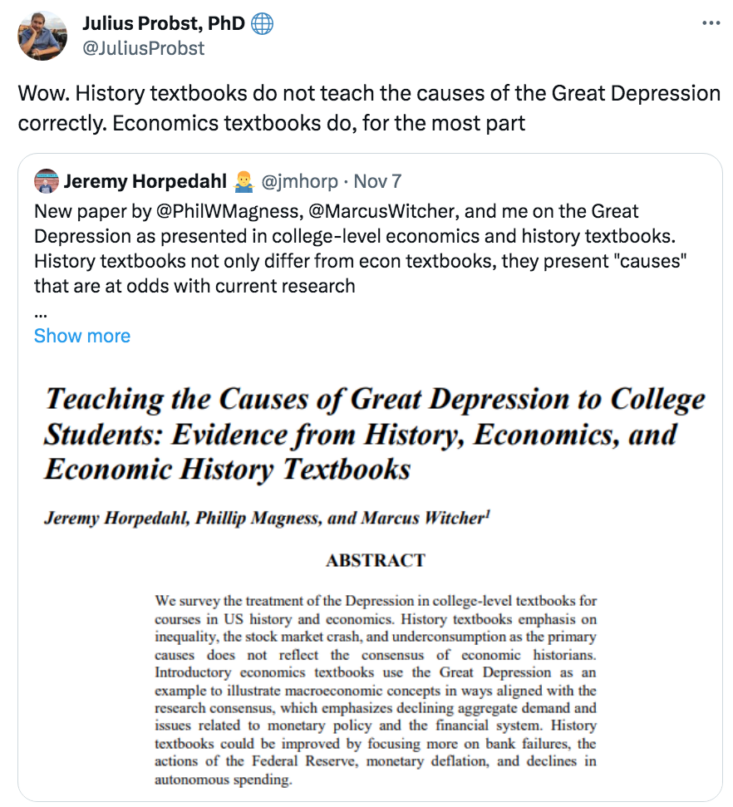

I as soon as wrote an complete ebook on the causes of the Nice Melancholy, specializing in the function of the interwar gold customary and FDR’s labor market insurance policies. In doing this analysis, I found that the query of causation is sort of difficult. One can search for proximate causes, reminiscent of unhealthy macroeconomic coverage, or deeper causes, reminiscent of institutional failures. (In idea, a melancholy may also be attributable to a pure phenomenon reminiscent of a plague or drought, however that was not the case with the Nice Melancholy. It was clearly a human created downside.) Though we don’t exactly know all the components that induced the Nice Melancholy, we’ve a fairly good concept as to which hypotheses usually are not useful.

Many individuals related the inventory market crash with the Melancholy resulting from the truth that it occurred at in regards to the time it grew to become obvious we had been sliding right into a deep hunch. Be aware that I stated “grew to become obvious”; the Melancholy truly started just a few months earlier than the crash. In October 1987, we had a pleasant check of the speculation that the inventory crash was a causal component within the Melancholy. A crash of virtually equal dimension occurred at nearly precisely the identical time of yr, after a protracted financial growth. Many pundits anticipated a melancholy, or not less than a recession. As an alternative, the 1987 inventory market crash was adopted by a booming financial system in 1988 and 1989.

After all it’s attainable to elucidate some distinction in final result to different components at play, however when the distinction is that this dramatic (booming financial system vs. the best melancholy in fashionable historical past), one has to wonder if the speculation is of any worth in any respect.

The identical is true of the inequality/underconsumption speculation. During the last 45 years, we’ve seen an attention-grabbing check of this idea. China has skilled an enormous enhance in financial inequality. Extra importantly, it has seen a few of the lowest ranges of consumption (as a share of GDP) ever noticed. Even decrease than different quick rising East Asian economies reminiscent of South Korea. Pundits have claimed that China’s consumption ranges are too low, and that too many sources are being dedicated to funding in areas of doubtful advantage.

Which will all be true. Maybe China ought to make investments much less and eat extra. Nevertheless it’s additionally clear that low ranges of consumption in China haven’t induced a Nice Melancholy. Certainly China’s had one of many quickest rising economies on this planet since 1978.

Once more, what impresses me about these two counterexamples (the US in 1987-89 and China since 1978) will not be that issues didn’t play out precisely because the historians may need anticipated primarily based on their idea of the Nice Melancholy. Fairly what impresses me is that the outcomes had been nearly 180 levels faraway from what may need been anticipated. That tells me that theories that inventory market crashes and underconsumption trigger depressions are primarily ineffective. They’re advert hoc explanations with no actual supporting financial idea and no predictive energy. Why ought to a inventory market crash trigger 25% of employees to cease working? What’s the mechanism? Why ought to excessive ranges of funding trigger actual GDP to say no by 30% over 4 years? What’s the mechanism? In the event that they haven’t any theoretical help and no predictive energy, then why ought to we care what historians imagine?

If you happen to get inventive sufficient you possibly can discover a causal mechanism working by combination demand. However then why not argue {that a} decline in combination demand induced the Nice Melancholy? In any case, that’s what truly did occur.

You would possibly say that it’s essential to know the reason for the Nice Melancholy. However why? If the theories provided by historians present no assist in understanding the fashionable world, then how are they of any use?

Extra broadly, I mistrust all theories of financial causation developed by non-economists (not simply historians). These theories are inclined to depend on “widespread sense”. Thus many common folks assume that nations are wealthy as a result of they’re large, or as a result of they’ve plenty of pure sources. (Maybe as a result of that idea form of suits the US.) However trying extra broadly, wealthy nations don’t are usually locations with giant populations or excessive ranges of pure sources. They are usually smaller nations in East Asia and Western Europe. The precise (institutional) components that designate the various wealth of countries are a lot more durable to see, and therefore are usually ignored by non-economists.

[ad_2]

Source link

:max_bytes(150000):strip_icc()/Health-GettyImages-1477523726-d9489f5e044241b097588b0636bf7561.jpg "Solar Poisoning: Indicators and Signs")

{kind=link}