[ad_1]

The macroeconomic results of structural reforms: An empirical and model-based strategy

Structural reforms embody a broad set of insurance policies that may completely alter the provision aspect of the financial system and create an atmosphere by which innovation can thrive. These insurance policies carry productive capability by strengthening incentives to extend manufacturing inputs or to make sure that these inputs are used extra effectively, thereby elevating productiveness. Eradicating cumbersome and anti-competitive regulation, growing enforcement of contracts and safety of property rights, and even designing incentives to spice up funding in analysis and growth (R&D) and innovation are all measures that may assist attain such targets. By enhancing productive capability, reforms additionally improve everlasting earnings, which favours combination demand. Whereas the long-run expansionary results of reforms on each GDP and potential output are uncontroversial, the short-term results on financial exercise, employment and inflation are much less apparent and require using a mannequin to be totally evaluated.

The prevailing literature usually gives two distinct approaches to the evaluation of the financial results of structural reforms. The primary relies on reduced-form proof (e.g. Barone and Cingano 2011, Lanau and Topalova 2016, Chemin 2020), which pursues the identification of a causal influence of the reforms, however doesn’t permit exploring the transition of the financial system in the direction of its new regular state. The second strategy relies on structural dynamic basic equilibrium fashions (e.g. Forni et al. 2012, Lusinyan and Muir 2013, Eggertsson et al. 2014, Varga et al. 2014, Cacciatore et al. 2016, Bilbiie et al. 2016), which permits for an correct evaluation of the short- and long-run dynamics of the consequences of the reforms. Nonetheless, the dimensions of the simulated reforms is often based mostly on working assumptions (e.g. “what would occur if the hole vis-a-vis finest practices was closed?”), with none underlying empirical estimate. The necessity to look at the trail from micro behaviour to macro outcomes, to uncover impediments and design efficient structural reforms, has been emphasised by Bartelsman et al. (2015).

In a current paper (Ciapanna et al. 2020), we attempt to bridge these two strands of literature and suggest an evaluation of the macroeconomic results of structural reforms based mostly on a three-step process. First, we quantify the reform by means of an acceptable indicator. Second, we estimate the reduced-form results of the reform on markups (a measure of agency’s market energy) and whole issue productiveness (TFP, a measure of effectivity in manufacturing). Third, we use such estimated results as exogenous shocks in a structural mannequin, to simulate every reform accounting for the transitional dynamics in the direction of the brand new regular state.

Results of the structural reforms

We take into account three reform packages: liberalisations within the regulated service sectors, incentives to innovation, and civil justice reforms. The liberalisation measures have been launched with the Decree Regulation ‘Salva Italia’ (L. 22 December 2011, n. 214) and with the Decree Regulation ‘Cresci Italia’ (L.24 January 2012, n. 1), by way of varied interventions that affected a number of sectors (e.g. vitality, transports, retail commerce {and professional} companies), and geared toward eradicating entry boundaries and different restrictions to aggressive markets. Fiscal incentives for funding in innovation have been included within the ‘Business 4.0’ Plan, launched in 2016 and subsequently renewed, which, among the many varied initiatives, included a collection of measures geared toward fostering funding (super-amortisation, so-called ‘new Sabatini’), and at boosting adoption of so-called ‘Business 4.0’ applied sciences (hyper-amortisation) and R&D expenditure (tax credit score on R&D). Lastly, the civil justice reform bundle, began in 2011, was geared toward tackling the big backlog of circumstances and the extreme size of trials within the Italian justice system. The actions undertaken, of various nature and significance, have been designed to scale back the variety of authorized disputes and to enhance the productiveness of the courts.

Microeconometric estimates, exploiting sectoral, geographical and firm-level sources of variation, point out that structural reforms can increase TFP whereas reducing companies’ market energy (Desk 1). Service liberalization have induced constructive results each on service sector TFP (+3.5%) and on the diploma of competitors, with a discount within the companies sector markup of about 1.1 share factors. Incentives to innovation result in a productiveness improve of round 1.4%. Lastly, civil justice system reforms result in a rise in TFP of 0.5%.

Desk 1 Abstract estimates

With a purpose to assess the macroeconomic influence of the three reforms, we simulate a multi-country two-sector dynamic basic equilibrium mannequin calibrated to Italy. The mannequin consists of two sectors – manufacturing and companies – which mix capital and labour with an exogenous TFP to supply output. Reforms geared toward growing the diploma of competitors in a sector are modelled as affecting the corresponding markup.

We deal with every of the three reforms as a separate exogenous shock. Following the proposed three-step process, the mannequin is fed with data on (i) the estimated influence of the reform on the artificial indicator thought-about (markup, TFP); and (ii) the implementation interval of the reform itself (see Desk 1, final two columns). Mannequin-based simulations present the ultimate step of the evaluation.

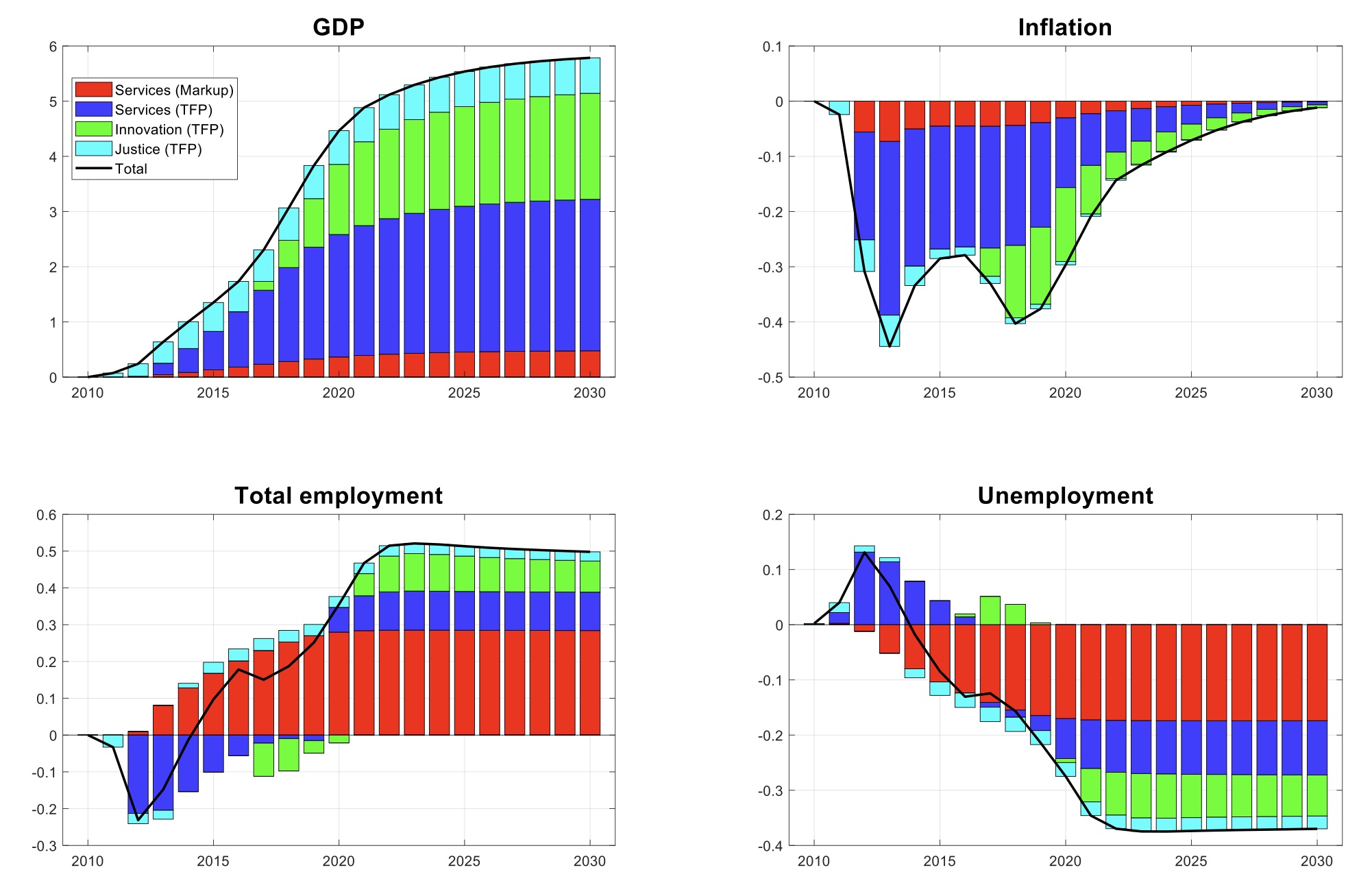

Determine 1 reviews the consequences of the reforms on the primary macroeconomic variables, over a 20-year interval. All reforms help GDP and have delicate deflationary results within the quick run, reflecting the supply-side growth induced by the rise in TFP and the discount in market energy within the service sector. The rise within the stage of GDP noticed within the first decade due to the only impact of the thought-about reforms could be practically 3%. An additional improve of about 3 share factors could be reached within the present, second decade. Making an allowance for the uncertainty surrounding our microeconometric estimates, the long-run improve in GDP (which might coincide with the one in potential output) would lie between 3.5% and eight%. Over the identical horizon, whole employment (right here expressed by way of hours labored) would improve by round 0.5%, whereas the unemployment fee would fall by about 0.4 share factors.

Determine 1 Macroeconomic results of the reforms

Be aware: Horizontal axis: years. Vertical axis: % deviations from baseline; for inflation, annualized share level deviations from baseline; for unemployment, share level deviations from baseline. GDP is evaluated at fixed costs.

Conclusion

Structural reforms play a key position in growing competitors and productiveness and due to this fact stimulating long-run financial progress, with non-negligible short-term results. Our outcomes are consistent with these obtained in research taking a look at comparable reforms utilizing completely different methodologies and approaches (e.g. OECD 2015, MEF 2016). Our evaluation considers solely a specific subset of the structural reforms carried out in Italy over the previous decade, and it intentionally excludes all different elements (i.e. exogenous shocks) that contemporaneously hit the Italian financial system in the identical interval. Certainly, coverage timing and sequencing, fiscal consolidation and exterior constraints may have an effect on the outcomes of structural reform programmes (Manasse and Katsikas 2018). Our outcomes additionally recommend that within the absence of the reforms, the dynamics of Italian TFP, GDP, and potential output would have been even weaker.

Authors’ Be aware: The views expressed on this column are these of the authors and shouldn’t be attributed to the Financial institution of Italy.

References

Barone, G and F Cingano (2011), “Boosting Development in Excessive-Debt Occasions: The position of service deregulation”, VoxEU.org, 6 December.

Bartelsman, E, F di Mauro and E Dorrucci (2015), “Eurozone Rebalancing: Are We on the Proper Monitor for Development? Insights from the CompNet Micro-based Knowledge”, VoxEU.org, 17 March.

Bilbiie, F, F Ghironi and M Melitz (2016), “The effectivity of entry, monopoly, and market deregulation”, VoxEU.org, 13 September.

Cacciatore, M and G Fiori (2016), “The Macroeconomic Results of Items and Labor Market Deregulation”, Evaluation of Financial Dynamics 20: 1-24.

Chemin, M (2020), “Judicial Effciency and Agency Productiveness: Proof from a World Database of Judicial Reforms”, Evaluation of Economics and Statistics 102: 49-64.

Ciapanna, E, S Mocetti and A Notarpietro (2020), “The Results of Structural Reforms: Proof from Italy”, Temi di Discussione (Working Papers) 1303, Financial institution of Italy (introduced at April 2022 Financial Coverage panel).

Eggertsson, G, A Ferrero and A Raffo (2014), “Can Structural Reforms Assist Europe?”, Journal of Financial Economics 61: 2-22.

Forni, L, A Gerali and M Pisani (2012), “Competitors within the companies sector and macroeconomic efficiency within the European nations: The case of Italy”, VoxEU.org, 3 April.

Lanau, S and P Topalova (2016), “The Influence of Product Market Reforms on Agency Productiveness in Italy”, IMF Working Papers 119.

Lusinyan, L and D Muir (2013), “Assessing the Macroeconomic Influence of Structural Reforms: The Case of Italy”, IMF Working Papers 22.

Manasse, P and D Katsikas (2018), “Financial Disaster and Structural Reforms in Southern Europe: Coverage Classes”, VoxEU.org, 1 February.

MEF – Ministry of Economic system and Finance (2016), “The Evaluation of the Macroeconomic Influence of Italy’s Reforms with a Give attention to Credibility”, Quest workshop, Italian Ministry of Economic system and Finance.

OECD (2015), Structural Reforms in Italy: Influence on Development and Employment.

Varga, J, W Roeger and J in ’t Veld (2014), “Development Results of Structural Reforms in Southern Europe: The Case of Greece, Italy, Spain and Portugal”, Empirica 41: 323-363.

[ad_2]

Source link

:max_bytes(150000):strip_icc()/Health-GettyImages-1477523726-d9489f5e044241b097588b0636bf7561.jpg "Solar Poisoning: Indicators and Signs")

{kind=link}