[ad_1]

Yves right here. This put up is written in a medical method, however it however makes an attempt to evaluate the influence of the hassle of the EU to divorce itself economically from the Russia. This appears to be like to be a fair-minded effort, given the resistance to candor about sanctions blowback. For example, it finds that Europe doesn’t have prepared substitutes for 3/4 of imports from Russia, primarily vitality and “different crucial and strategic uncooked supplies.” Oopsie.

By Francesco Di Comite, Chief Economist workforce member, DG GROW (Inner market, trade, entrepreneurship and SMEs) European Fee and Paolo Pasimeni, Senior Affiliate Brussels Faculty Of Governance – Vrije Universiteit Brussel; Deputy Chief Economist – DG Inner Market and Trade European Fee. Initially printed at VoxEU

The European financial system was nonetheless recovering from the influence of the Covid-19 pandemic when the Russian invasion of Ukraine triggered new financial disruptions, highlighting the significance of publicity to geopolitical dangers and the vulnerability of worldwide worth chains. This column examines the exposures and dependencies of the EU financial system on the time of the invasion and the large adjustment going down to decouple from Russia. Whereas the openness and suppleness of the EU financial system allowed companies to reorganise their provide chains in a comparatively quick time, this adjustment might have structural impacts on the competitiveness of European trade.

The EU is among the important actors in international commerce and one of many driving forces of worldwide worth chains integration. This has allowed the European financial system to reap the advantages of globalisation, specialize in excessive value-added processes, and enhance its productive effectivity. But, a rigidity between effectivity and resilience has emerged lately. When in early 2022 the European financial system was nonetheless recovering from the influence of the pandemic, the Russian invasion of Ukraine triggered new financial disruptions, highlighting the significance of publicity to geopolitical dangers and the vulnerability of worldwide worth chains.

On this column, we analyse these vulnerabilities and deal with the endeavour of the European financial system to decouple from Russia. In doing so, it enhances quite a few current research which have analysed the implications of the sanctions and post-invasion disruptions in Russia (Demertzis et al. 2022) and throughout the globe (Borin et al. 2022, Langot et al. 2022, Attinasi et al. 2022, Ruta 2022, OECD 2022, IMF 2022).

Decoupling from a structurally related commerce companion requires a number of efforts. In a brand new paper (Di Comite and Pasimeni 2023), we illustrate the massive ongoing adjustment that the European financial system goes via, figuring out exposures and the unwinding of dependencies in the middle of 2022. We have a look at them from a risk-assessment perspective, specializing in dependencies and associated vulnerabilities, particularly on imported commodities.

The importance of Russia as a commerce companion for the EU was amplified by the focus of its enter in key provide chains. Power-producing commodities and different crucial and strategic uncooked supplies (CRSMs; see European Fee 2020, 2023) have a low diploma of substitutability and a restricted variety of international suppliers. They account for greater than three quarters of all EU imports from Russia. For almost all of those inputs, imports from Russia have been falling considerably in the middle of the 12 months, signalling a reconfiguration of provide chains in the direction of different sources.

On the Russian facet, the EU was the main commerce companion, offering an enormous number of funding items and high-tech merchandise. The sectoral construction of commerce means that China represents for Russia a attainable different to the EU, as a result of it’s a main exporter in these sectors for which the EU was one the principle companion for Russia. These are usually manufacturing of equipment and gear, laptop and electronics, fabricated metallic and plastic merchandise, chemical substances and textiles.

Gross Commerce flows

On the time of the invasion, the EU was extremely uncovered to the import of Russian commodities, notably fossil fuels and important uncooked supplies, however knowledge present that it regularly managed to scale back such publicity over the course of 2022. Utilizing a singular, high-frequency dataset primarily based on customs knowledge, we doc a sudden and sizeable discount of EU exports to Russia simply after the invasion. Imports adjusted extra regularly due to the low diploma of substitutability of fossil fuels and important uncooked supplies. Furthermore, they grew to become way more costly within the weeks after the invasion.

This has led to the EU accumulating a further bilateral commerce deficit vis-à-vis Russia of roughly €67 billion in 2022, in contrast with the identical interval in 2021. Such extra commerce surplus for Russia corresponds to roughly 3.3% of its GDP and has in all probability been one of many components behind the preliminary strengthening of its forex. But, with a sustained discount in volumes of fossil gas imports, by the tip of 2022, the EU managed to cease, and even began to revert, this deficit accumulation vis-à-vis Russia.

Determine 1 Change within the EU–Russia commerce stability with respect to 2021 (€ billion, five-week transferring common)

Strategic Dependencies

Lately, the European Fee has proposed methodologies to establish ‘strategic dependencies’ – merchandise for which the EU depends on a extremely concentrated set of overseas suppliers and has restricted home manufacturing capability (European Fee 2021, 2022) – and CSRMs – necessary commodities with a excessive provide threat (European Fee, 2020, 2023). We have been capable of establish 12 strategic dependencies vis-à-vis Russia (of not less than €100 million in imports) and 19 CRSMs. With a number of exceptions (nickel mattes and fuels for nuclear reactors), imports of merchandise for which the EU had a dependency on Russia decreased considerably over the course of 2022, on common by 20 proportion factors in market shares. The availability of 11 of the 19 CRSMs decreased by 50% or extra.

Determine 2 EU dependencies on Russia: Market share modifications between 2021 and 2022

Power

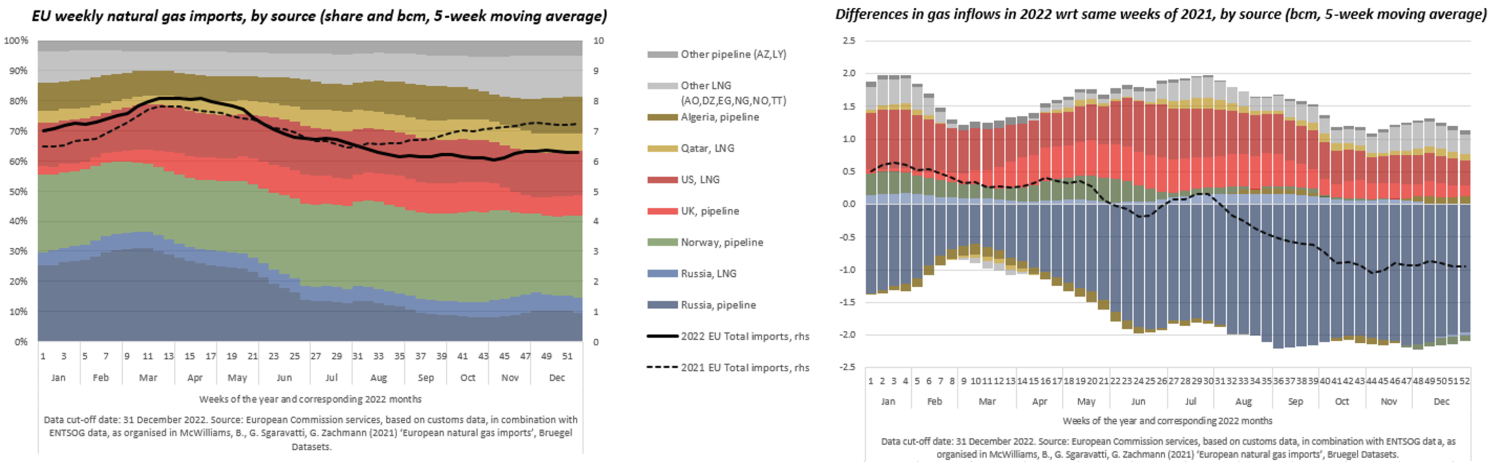

Power merchandise, and fossil fuels particularly, have been key inputs for the EU financial system sourced from Russia (€110 billion in 2021, 74% of the entire vitality import). Pipeline gasoline imports alone account for multiple third of all EU vitality imports from Russia, and in February 2022 they accounted for greater than 30% of all EU gasoline inflows. Since at present gasoline is the marginal supply used to stability the inner vitality system, its value evolution determines the costs of the complete EU vitality and electrical energy techniques.

The overall quantity of pipeline gasoline import from Russia fell by one third in 2022 in comparison with 2021, whereas total EU imports of gasoline in 2022 remained at roughly the identical stage, due to diversification into different sources of liquefied pure gasoline (LNG) – the US particularly. Nonetheless, LNG import costs are 46% dearer than pipeline gasoline import costs, with Russian LNG being the costliest (Russian LNG import costs within the EU being 60% above common gasoline import costs) and US LNG being solely barely cheaper (50% above common gasoline import costs). A structural shift from pipeline to LNG gasoline sources might thus suggest for the European trade a substantial lack of competitiveness.

Determine 3 Weekly pure gasoline flows (pipeline and LNG) into the EU by supply in 2022 and 2022-2021 differentials

Conclusion

The Russian invasion of Ukraine has led to a everlasting adjustment of EU provide chains, with a progressive decoupling from Russia. On the one hand, the Russian financial system is regularly dropping one in every of its important overseas sources of revenue. The extent to which Russia can substitute the EU with different commerce companions stays an open query. However, the European financial system is performing a sizeable adjustment in its provide chains, particularly for key uncooked supplies and vitality merchandise.

All in all, the European financial system demonstrated substantial resilience to the shock. Our evaluation exhibits that the openness and suppleness of the EU financial system allowed companies to reorganise their provide chains in a comparatively quick time. But, this adjustment can have structural impacts on the competitiveness of the European trade, given the necessity to flip to second-best provide chain configurations. If persistent, the comparatively larger value of key inputs might lead to losses of market shares, particularly in sectors key to the inexperienced transition.

The unprecedented nature of this shock has prompted a mirrored image when it comes to resilience, of enterprise fashions, and of provide chains that’s not restricted to short-term fixes. This disaster stress-tested the resilience and skill to regulate of the European financial system. The problem is now to make sure the sustainability and competitiveness of the rising provide chain configurations.

See authentic put up for references

[ad_2]

Source link

:max_bytes(150000):strip_icc()/Health-GettyImages-1477523726-d9489f5e044241b097588b0636bf7561.jpg "Solar Poisoning: Indicators and Signs")

{kind=link}