[ad_1]

“This isn’t 2008”: That was the mantra of Biden administration officers on Monday as they sought to reassure buyers and the general public {that a} regulatory takeover of two failed banks and rescue of their depositors, together with newly applied safeguards, can be sufficient to avert a broader disaster within the monetary system.

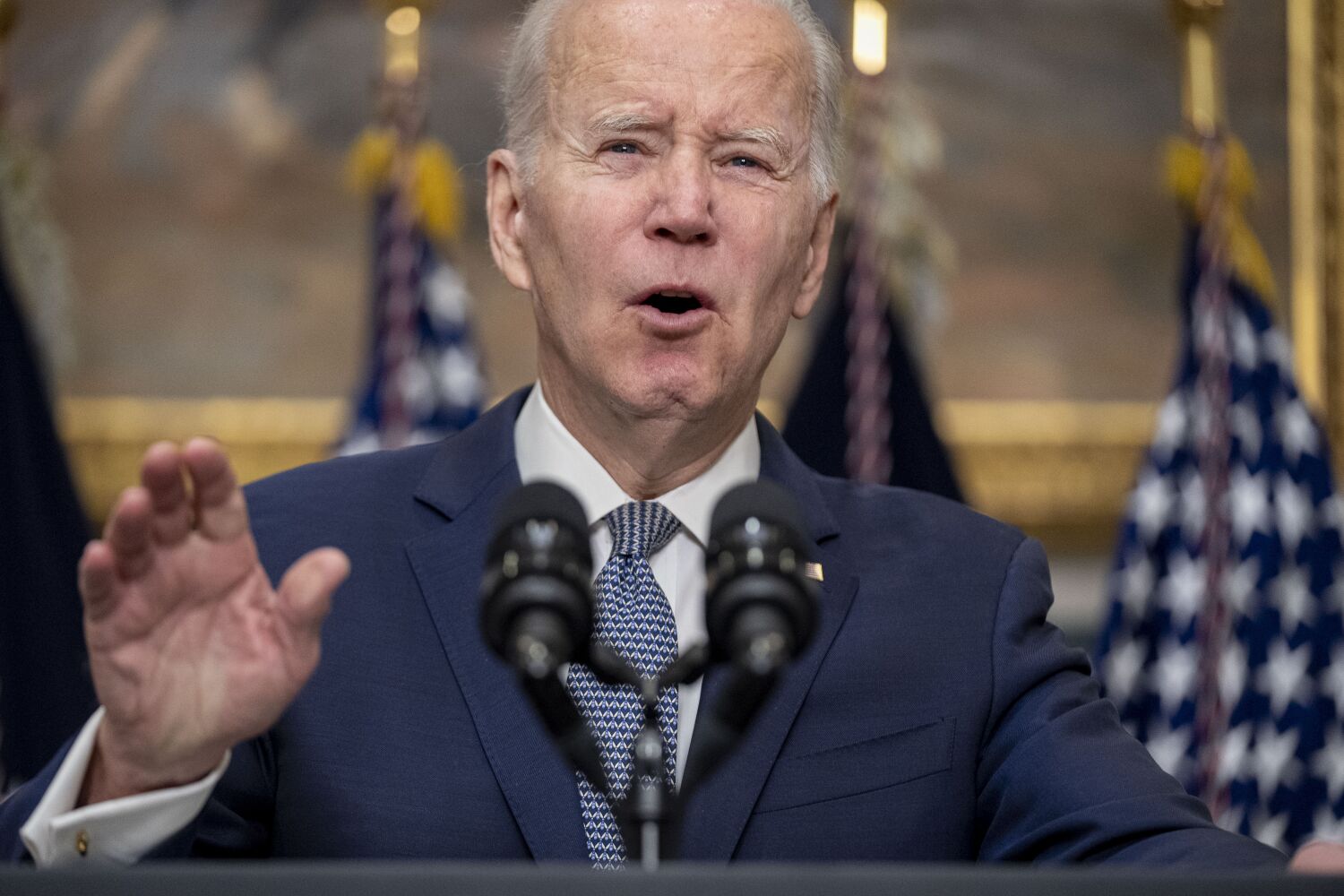

As shares opened a jittery day of buying and selling that introduced massive losses for some regional banks, notably San Francisco-based First Republic, President Biden declared the underlying banking infrastructure “protected and safe” from aftershocks led to by the deadly run on Silicon Valley Financial institution.

“Individuals can have faith that the banking system is protected. Your deposits can be there while you want them,” Biden mentioned in remarks on the White Home earlier than leaving for a three-day go to to California and Nevada.

After a weekend spent warning of domino results and mass layoffs, enterprise capitalists and hedge fund managers had largely reward for the plan to ensure deposits at Silicon Valley Financial institution and Signature Financial institution by invoking a “systemic threat exception” permitting regulators to backstop even deposits too massive to qualify for federal insurance coverage.

“The #1 factor we should always be grateful for is decisive motion from the US Authorities at each stage of this: the White Home, Treasury, FDIC, the Fed, Congress, and California leaders who stepped up large,” tweeted Garry Tan, chief govt on the Silicon Valley startup accelerator Y Combinator.

The plan introduced by the U.S. Treasury, the Federal Reserve Financial institution and the Federal Deposit Insurance coverage Corp. additionally included a brand new instrument to stop the unfold of financial institution failures. Underneath it, banks whose steadiness sheets are hobbled by excessive rates of interest will have the ability to entry liquidity within the type of Fed loans in opposition to their affected property.

As a part of the FDIC’s takeover of Silicon Valley Financial institution, its prime executives have been fired, and a brand new chief govt was appointed: Tim Mayopoulos, a software program govt who helped mortgage assure firm Fannie Mae navigate the monetary disaster and served as its chief govt from 2012 to 2018. Monetary regulators are actually reviewing whether or not Silicon Valley Financial institution, primarily based in Santa Clara, had performed the required planning and stress testing because the Fed raised rates of interest beginning final 12 months, in keeping with Bloomberg.

The inventory market as a complete appeared unperturbed by lingering questions over the well being of the banking system, ending buying and selling Monday basically flat.

However markets have been gradual to dismiss the chance that liquidity points may crop up at different medium-size banks, placing their depositors and particularly their buyers in danger, and widening the circle of financial fallout. Banks took a average hit, with regional financial institution shares down 7.7% on Monday to their lowest degree since June 2020.

Midsize establishments with buyer bases much like Silicon Valley Financial institution’s — wealthy folks — obtained pounded. Hit hardest was First Republic Financial institution. Its inventory dived 62% on Monday, whilst First Republic Financial institution officers mentioned liquidity was not a difficulty.

That’s but to be absolutely decided. First Republic’s enterprise mannequin is much like Silicon Valley Financial institution’s. They each serve the profitable market of Silicon Valley entrepreneurs, executives and firms, and each are struggling asset markdowns as rates of interest rise. However First Republic has much more of its property in jumbo mortgages on high-priced houses, and relies upon much less on the banking enterprise of particular person startup corporations.

Regulators have been working time beyond regulation since late final week. On Friday, after a day by which clients tried to withdraw $42 billion in funds, the FDIC seized management of Silicon Valley Financial institution, which held greater than $200 billion in property as of the tip of 2022. Its failure was the biggest since 2008. Then, over the weekend, regulators shuttered Signature Financial institution after they decided it additionally offered a systemic threat.

Regardless of failing to seek out patrons instantly ready to take over their property and liabilities, the Treasury Division introduced Sunday that clients at each banks, together with those that had funds exceeding the $250,000 federal insurance coverage restrict, would have entry to their funds starting Monday.

In his remarks Monday, Biden promised that taxpayers wouldn’t bear the prices and the cash would as an alternative come from charges that banks pay into the federal Deposit Insurance coverage Fund.

Biden additionally vowed to carry accountable these liable for the collapse and mentioned the financial institution’s shareholders wouldn’t be protected.

Biden blamed the financial institution collapses on former President Trump’s 2018 determination to loosen banking guidelines enacted within the wake of the 2008 monetary disaster.

“Sadly, the final administration rolled again laws,” Biden mentioned.

The president mentioned he deliberate to ask Congress and financial institution regulators to revive the Obama-era guidelines.

Democrats have been divided concerning the 2018 overhaul of the 2010 Dodd-Frank Wall Avenue Reform and Client Safety Act, with extra liberal lawmakers together with Sen. Elizabeth Warren (D-Mass.) warning the adjustments would put “American customers at larger threat.”

Sixteen Senate Democrats and unbiased Angus King of Maine, who normally votes with Democrats, joined Republicans to vote for the invoice. Within the Home, 33 Democrats joined all however one Republican in approving the measure. Florida Gov. Ron DeSantis, a potential 2024 presidential candidate who was a member of the Home on the time, was among the many Republicans who voted for the invoice.

Though there was broad bipartisan help for the rescue of Silicon Valley Financial institution and Signature Financial institution clients Monday, some Republicans took the chance to slam the Biden administration for what they referred to as a “bailout.” They included presidential candidate Nikki Haley and Missouri Sen. Josh Hawley.

[ad_2]

Source link

| The Gateway Pundit")

{kind=link}