[ad_1]

“A new product that provides buyers full draw back safety: Traders within the $7.5 trillion ETF universe can now put cash behind the Innovator Fairness Outlined Safety ETF, which started buying and selling below the ticker TJUL on Tuesday. The providing comes from Innovator Capital Administration, which launched the primary so-called buffer ETFs, additionally typically known as defined-outcome funds, in 2018.” –Bloomberg

Let’s get this out of the best way: I dislike any product that exchanges a portion of your potential positive aspects in change for draw back safety.

Let’s focus on why.

At first, merchandise like these are wholly pointless. No less than, if you’re a wise investor who does the fitting issues: Arrange a monetary plan, handle your personal conduct, interact in long-term considering, and keep away from reacting to the limitless day by day noise that markets + media generate.

Second, observe Charlie Munger’s recommendation and invert the gross sales pitch: 70% of the upside (you quit 16.62% per 12 months for two years) with not one of the draw back sounds engaging – except you consider what you’re actually giving up and getting in change.

Would you settle for a commerce the place for ~32% of the upside, you’re free of having to handle your personal conduct? That sounds fairly costly for one thing that ought to value you a) nothing should you do it your self, or 2) 50-100 bps should you work with an advisor.

That appears like a horrible deal to me.

Third, while you personal a broad index of equities, the upside compounds over the long term whereas the drawdowns are non permanent. Giving up everlasting positive aspects to keep away from impermanent drops looks like an terrible change.

My apparent bias is that my advisory agency costs purchasers to create monetary plans and handle their property. However simply do the maths: Would you like to surrender 67 foundation factors (RWM’s dollar-weighted common payment is ~0.67%) or would you like to surrender 30% of your positive aspects PLUS pay an annual 0.79% payment for the TJUL ETF? It’s the advisor’s job to forestall purchasers from partaking within the type of dangerous funding conduct that drawdowns usually trigger; I can not see how buying and selling that for >30% of the upside makes any sense.

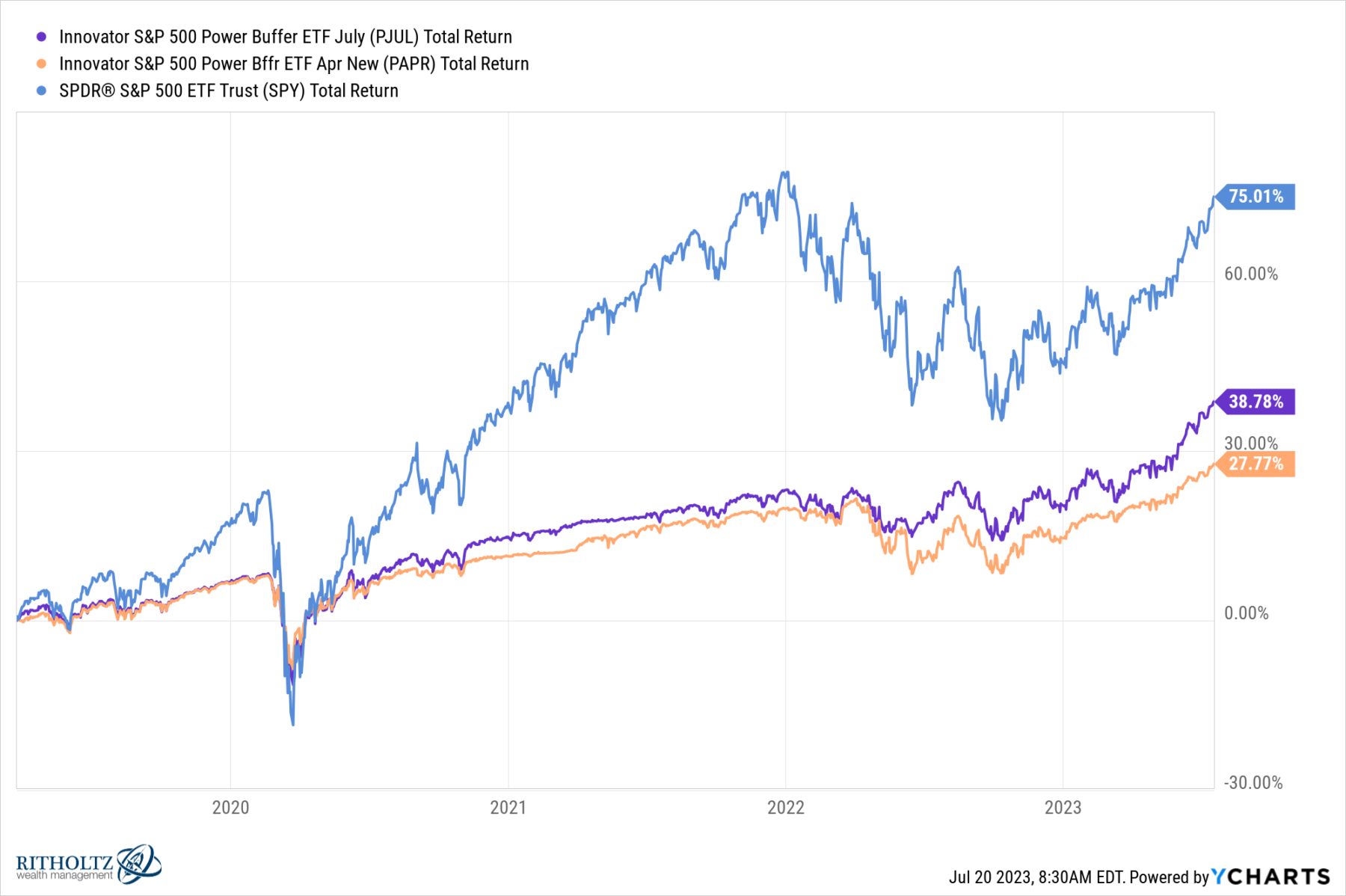

Innovator, the agency behind TJUL, manages “greater than 50 buffer funds which have collectively drawn over $12 billion in property since 2018. . . Among the many largest automobiles are the Innovator S&P 500 Energy Buffer ETF (PAPR), totaling about $687 million in property, and the Innovator S&P 500 Energy Buffer ETF (PJUL), which has roughly $834 million in property.”

These funds have a beginning upside cap of 14.28% versus TJUL’s 16.62%; the chart above reveals how they’ve accomplished 12 months so far: Up 11.5% and 15.1% respectively this 12 months, versus 19.9% for SPY. Since inception (March 2019), they’re up 27.8% and 38.8% respectively, versus 75% for the SPY S&P 500 ETF over the identical interval. (Chart after the leap).

The efficiency numbers reveal this can be a horrible trade-off for the typical retail investor.

See additionally:

Innovator TJUL

Innovator PAPR

Innovator PJUL

Supply:

Wall Avenue Will get New ETF Providing 100% Draw back Safety

By Vildana Hajric, and Emily Graffeo

Bloomberg, July 18, 2023

PJUL, PAPR, SPY March 25 2019 to July 10, 2023 (yesterday’s market shut)

[ad_2]

Source link

{kind=link}