[ad_1]

Over the previous decade, fintechs and Huge Techs started to supply monetary companies initially outdoors the banking system, with a number of lately gaining approval to function banks in Asia, Europe, and within the US. These developments have been supported by secular traits – akin to the provision of cellular gadgets – and turbocharged by the Covid-19 pandemic.

Tech corporations fall throughout the spectrum of ‘non-financial firms’ (NFCs) which have sought a banking license. In some jurisdictions, banking authorities have historically curtailed sure NFCs – akin to large business and industrial corporations – to personal a financial institution. They’ve discouraged such affiliations because of prudential considerations surrounding potential conflicts of curiosity, competitors points, contagion and systemic dangers, and the capability to conduct group huge supervision (Acharya and Rajan 2020, Blair 2004, Wilmarth 2020).

Why have some prudential authorities allowed these new courses of NFCs –– together with Huge Techs and fintechs –– to personal banks? Are the supervisory considerations concerning the affiliation between banks and massive corporates related within the context of tech corporations’ pursuit of a banking license? What prudential safeguards might be launched to attenuate the perceived dangers with out undermining the potential advantages their entry could convey to society? In a latest paper (Zamil and Lawson 2022), we delve into these questions by framing the dialogue as a part of a longstanding debate on whether or not to permit the blending of banking and commerce in a contemporary, digital context.

Advantages and dangers of tech-owned banks

Tech corporations usually are higher positioned to ship on some authorities’ coverage goals of selling inclusion and fostering competitors in comparison with conventional NFCs. The proliferation of cellular gadgets, along with their deployment of superior know-how and user-friendly apps, can allow tech corporations to succeed in a broader vary of underserved shoppers and to carry out varied points of the banking enterprise extra effectively and at a less expensive value. Tech corporations may have extra entry to and larger means in evaluating client knowledge (Feyen et al. 2021). This may increasingly assist with assessing borrower creditworthiness, facilitating higher pricing and enhancing product choices, which can enhance client outcomes.

Nonetheless, some tech corporations could pose related – if not larger – dangers as conventional NFCs throughout 5 threat dimensions.1

- Conflicts of curiosity: A financial institution could also be compelled to interact in transactions at extra beneficial phrases with its company guardian or to affiliated non-financial entities managed by the identical guardian, which may undermine its energy.

- Competitors: Massive NFCs could use their present buyer base, monetary sources, and market energy to subsidise their banks’ actions and acquire market share, which may erode competitors.

- Contagion and systemic threat: Affiliations between NFCs and banks could also be such that monetary misery at one could trigger misery on the different, risking spillover results from the monetary sector to the actual financial system or vice versa.

- Consolidated supervision: Banks owned by NFCs could also be a part of massive company teams with a number of subsidiaries and associates, which may pose a problem for supervisors to carry out group-wide supervision.

- Mum or dad firm assist: Throughout authorisation, supervisors think about the guardian’s means to supply monetary assist to the financial institution. Just like business NFCs, the monetary capability of tech corporations varies with a number of persevering with to report web losses, as they increase their digital footprint.

A framework to evaluate tech corporations’ threat profile

To find out their threat traits and to assist inform coverage choices, we disaggregate tech corporations that have interaction in monetary actions into three teams and examine them in opposition to business and industrial NFCs throughout 5 threat components (Desk 1):

- ‘Stand-alone fintechs’ are corporations whose monetary actions are carried out solely or primarily by their banking entity.

- ‘Diversified fintechs’ are corporations who have interaction in a broader vary of monetary companies by varied channels, together with the guardian entity degree, their banking subsidiary and different non-bank subsidiaries, joint ventures and affiliated firms.

- ‘Huge Techs’ are corporations with core non-financial companies in social media, web search, software program, on-line retail and telecoms, who additionally supply monetary companies as a secondary enterprise line (Monetary Stability Board 2020).

Desk 1 NFCs and financial institution possession – potential dangers

Supply: FSI evaluation

Amongst tech corporations, Huge Techs pose the best dangers, adopted by massive, diversified fintechs (Carstens et. al 2021, Crisanto et al. 2021a).3 This evaluation is predicated on the relative complexity of their organisational buildings, the size of their monetary and non-financial strains of companies, the scale of their captive consumer networks, abundance of information and monetary sources, which, collectively can have advanced interactions with their in-house financial institution. These attributes can intensify potential supervisory considerations throughout the primary 4 threat dimensions. Nevertheless, Huge Techs have larger market entry – in comparison with different tech corporations – offering them with extra flexibility to supply monetary assist to their banking entity.

The regulatory panorama for tech-owned banks

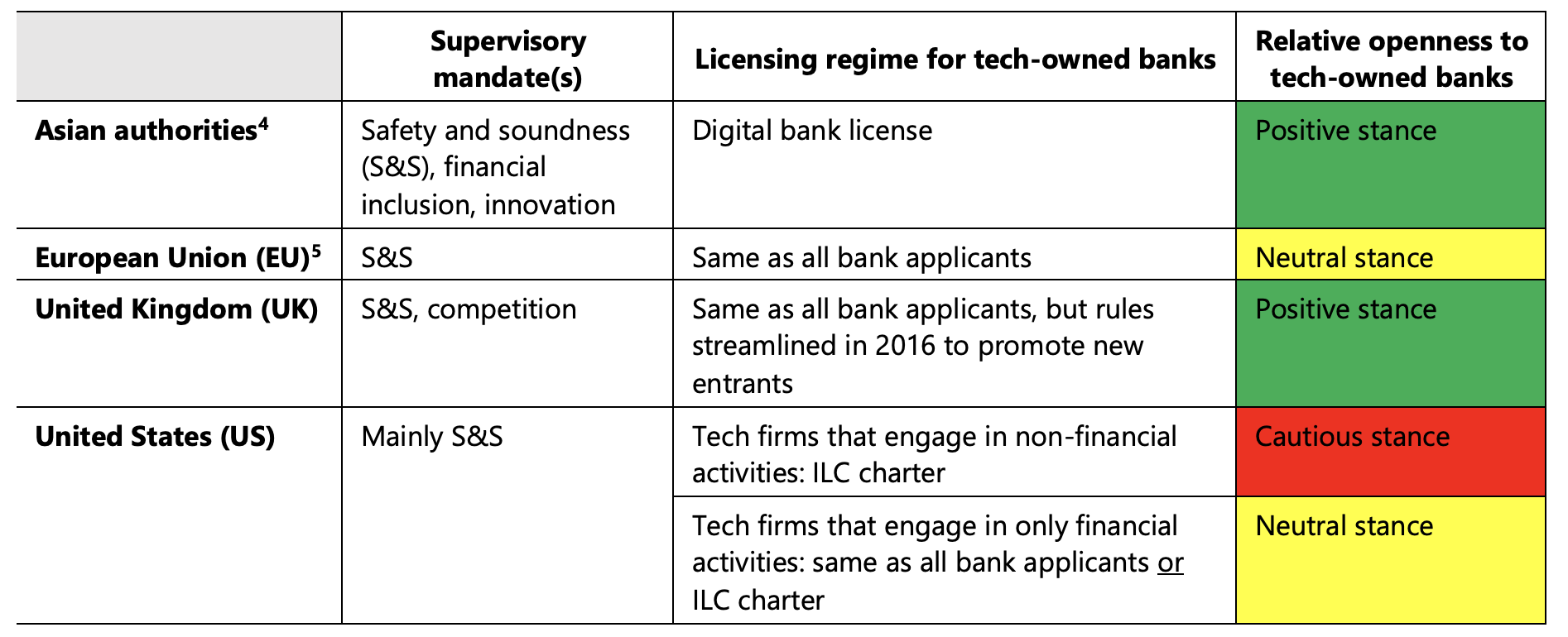

Banking supervisors are guided by a set of core ideas issued by the Basel Committee on Banking Supervision, which give requirements for the regulation and supervision of banks (Basel Committee on Banking Supervision 2012). One in all these ideas outlines licensing necessities, which oblige supervisors to prescribe minimal capital ranges and assess, amongst different points, the applicant’s possession construction, governance, main shareholders, and the guardian’s means to supply monetary assist. Regardless of an identical start line, authorities apply various licensing regimes to tech-owned financial institution candidates (Desk 2).

Desk 2 Supervisory mandates, licensing regimes and regulatory posture

Supply: FSI evaluation

Authorities with mandates that embody monetary inclusion, technological innovation or competitors seem extra inclined to license tech-owned banks. Amongst these jurisdictions, some have developed digital financial institution licenses (varied Asian jurisdictions), whereas others streamlined their normal financial institution licensing course of to advertise competitors (UK). In jurisdictions the place mandates are extra narrowly centered on ‘security and soundness’, they are typically coverage impartial (EU) or extra cautious (US) in licensing tech-owned banks. EU supervisors use their present financial institution licensing course of to evaluate tech-owned candidates. Within the US, fintechs that have interaction in solely monetary actions could apply for a conventional financial institution constitution, however tech corporations that have interaction in any non-financial exercise (akin to Huge Techs) should get hold of an ‘industrial mortgage firm’ (ILC) constitution.6

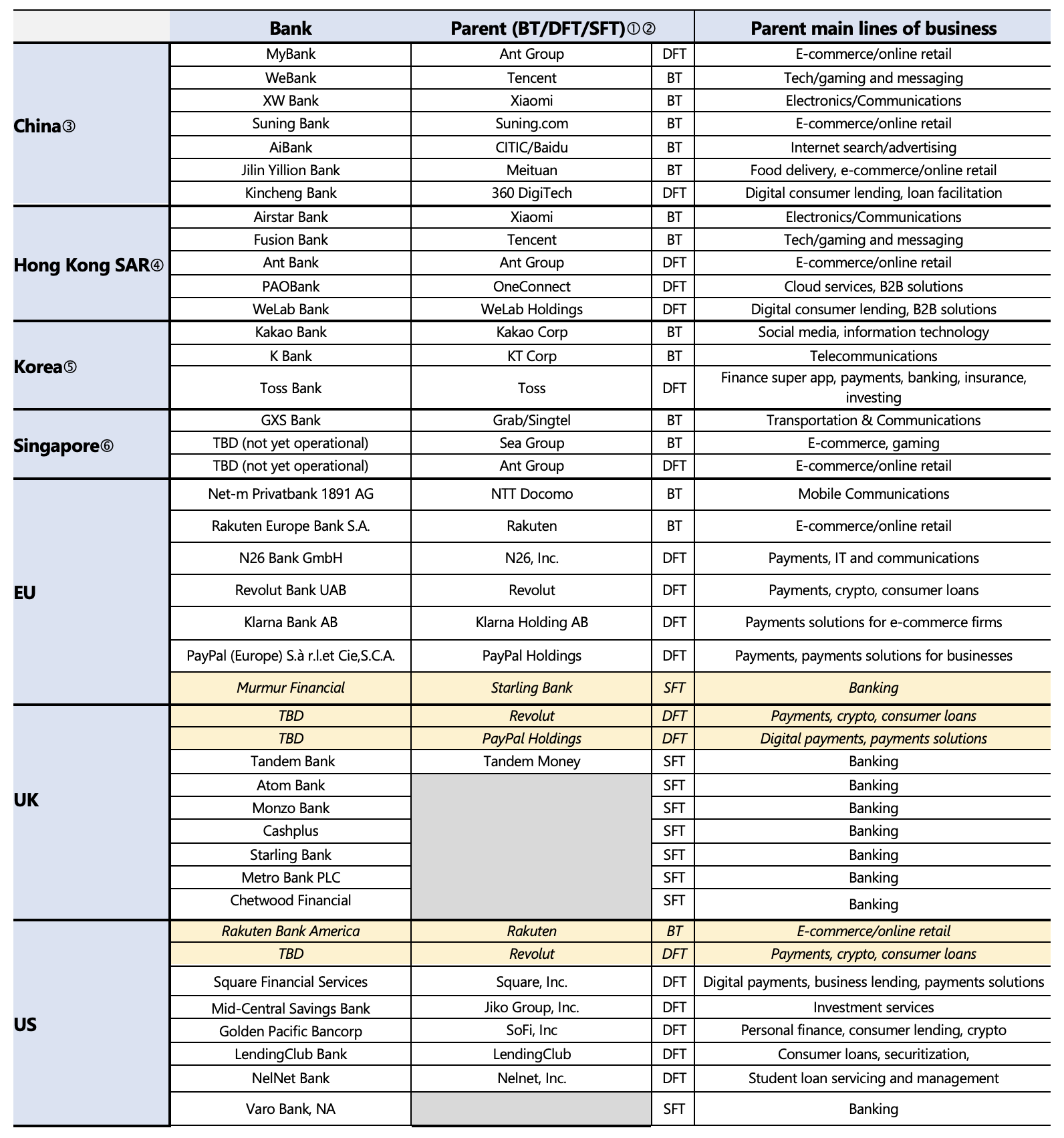

Desk 3 supplies a snapshot of tech corporations with accepted or pending financial institution licenses in chosen jurisdictions.

Desk 3 Tech corporations with accepted or pending banking licenses – possession and principal enterprise strains7

Supply: Firm regulatory filings; FSI evaluation.

Whereas the US, arguably, imposes probably the most onerous licensing necessities, Asian authorities which are comparatively ‘tech-friendly’, purpose to tailor their licensing necessities to the construction and enterprise fashions of those new entrants.8 Amongst varied quantitative and qualitative necessities, some provisions are noteworthy:

- Measures designed to scale back systemic threat: All jurisdictions require tech-owned banks to develop an exit plan in case of failure, whereas some impose increased capital necessities on them.11 The US prohibits an ILC chartered financial institution from getting into into any contract for companies materials to its operation with the tech guardian or their affiliated firms.10

- Consolidated supervision: China and Hong Kong require tech-owned mother and father assembly sure standards to consolidate all monetary entities throughout the group right into a monetary holding firm to facilitate group-wide supervision.

- Prohibition on overlapping boards and senior executives: The US prohibits guardian firms from having a majority board illustration on the ILC financial institution, whereas limiting the hiring of senior executives on the ILC financial institution if the person has been related to the tech guardian in previous three years. These measures, along with complete guidelines governing transactions between a financial institution and its associated events, could assist to minimise conflicts of curiosity.

- Competitors: China prohibits Huge Techs with financial institution subsidiaries from abusing their market energy or technological superiority. Korean laws restrict any firm in violation of anti-monopoly guidelines over the previous 5 years from proudly owning greater than 10% of a financial institution. No different jurisdictions have specific competition-related provisions of their licensing frameworks, however efforts are underway to establish ‘dominant’ corporations and impose necessities to deal with competitors points (Crisanto et al. 2021b).

- Mum or dad firm assist: Whereas all jurisdictions assess tech mother and father’ means to financially assist its financial institution subsidiary, only some require tangible proof of guardian firm assist. China requires the tech guardian to be worthwhile for a interval of not less than two consecutive years, whereas the US requires the tech guardian and/or principal shareholders to pledge property or safe a line of credit score to display assist to the subsidiary financial institution.

Conclusions

Tech corporations’ entry into the banking system could advance varied public coverage targets, nevertheless it additionally introduces new dangers and amplifies older ones. New dangers – significantly for Huge Techs and diversified fintechs – stem from their scalable enterprise fashions which are premised on extracting knowledge from their massive and captive consumer base that may be leveraged as they enter banking. These options could irritate conventional considerations when banks affiliate with massive NFCs. Furthermore, a number of tech corporations stay unprofitable, elevating questions on their means to assist their in-house financial institution.

Whereas authorities impose varied qualitative and quantitative licensing necessities, they don’t seem to be all the time tailor-made to tech corporations’ threat traits. In most jurisdictions, authorities purpose to observe the precept of ‘similar exercise, similar threat, similar regulation’. Nevertheless, the identical banking exercise carried out by sure tech corporations could not essentially result in the identical dangers (Restoy 2021). These developments name for differentiated licensing guidelines amongst tech corporations.

The American rapper and music producer will.i.am as soon as stated, “Magazines and web sites are the gatekeepers of what folks suppose hip-hop is, however they really find yourself limiting what hip-hop might be”. The entry of tech corporations in banking supplies supervisory authorities with a singular alternative to steer the worldwide banking panorama. Their problem is to strike a stability between setting financial institution licensing necessities which are commensurate with tech corporations’ inherent threat traits and prescribing overly onerous guidelines that protect incumbents from wholesome competitors which may hinder technological improvements within the provision of monetary companies.

Authors observe: The views expressed are these of the authors and don’t essentially mirror these of their employers, together with the Financial institution for Worldwide Settlements or the Basel-based normal setters.

References

Acharya, V and R Rajan (2020), “Do we actually want Indian companies in banking?”, November.

Basel Committee on Banking Supervision (2012), “Core ideas for efficient banking supervision”, September.

Blair, C (2004), “The blending of banking and commerce: Present coverage points”, FDIC Banking Evaluation 16(3 and 4): 97–120.

Carstens, A, S Claessens, F Restoy, and H S Shin (2021), ”Regulating Huge Techs in finance”, BIS Bulletin 45, August.

Crisanto, J C, J Ehrentraud, and M Fabian (2021a), “Huge Techs in finance: Regulatory approaches and coverage choices”, FSI Briefs no 12, March.

Crisanto, J C, J Ehrentraud, F Restoy, and A Lawson (2021b), “Huge tech regulation: What’s going on?”, FSI Insights on Coverage Implementation 36, September.

Feyen, E, J Frost, L Gambacorta, H Natarajan, and M Saal (2021), “A coverage triangle for Huge Techs in finance”, VoxEU.org, 23 October.

Monetary Stability Board (2020), “BigTech corporations in finance in rising market and creating economies – market developments and potential monetary stability implications”, 12 October.

Restoy, F (2021): “Fintech regulation: The right way to obtain a degree taking part in subject”, FSI Occasional Papers 17, February.

Wilmarth, A (2020), “Re: FDIC Docket RIN 3064-AF31 – Discover of proposed rulemaking: “Mum or dad firms of business banks and industrial mortgage firms”, 85 Fed. Reg. 17771, 10 April.

Zamil R and A Lawson (2022), “Gatekeeping the gatekeepers: when bigtechs and fintechs personal banks- advantages, dangers and coverage choices”, FSI Insights on coverage implementation No 39, January.

Endnotes

1 For added dialogue on the expansion of fintech and the dangers they pose to monetary stability, consult with the IMF’s April 2022 World Monetary Stability Report, Chapter 3.

2 The classification of “low”, “reasonable” and “excessive” threat are based mostly on the authors’ judgment of the inherent dangers related to tech corporations throughout the required threat dimensions. Inside a gaggle of tech corporations, there could also be variations in threat dispersion that can’t be captured by this generalised methodology.

3 Stand-alone fintechs pose the least prudential considerations amongst tech corporations throughout the primary 4 threat dimensions because of their small measurement and lack of a fancy organizational construction. Nonetheless, they nonetheless pose varied challenges which must be thought of in the course of the licensing course of, together with the viability of their enterprise fashions, the adequacy of threat administration, and the flexibility of sponsors to assist the financial institution.

4 Asian authorities lined in our paper embrace China, Hong Kong, Korea, and Singapore

5 The mandate of the only supervisory mechanism of the European Central Financial institution is used as a proxy for the supervisory mandate of the EU.

6 The ILC constitution was initially developed for commercial-industrial NFC financial institution homeowners, however supplies scope for authorities to tailor necessities for tech-owned financial institution mother and father.

7 This desk isn’t an all-inclusive checklist and supplies a particular overview of accepted or pending banking licenses.

8 For example, whereas China has been on the forefront in encouraging tech corporations to acquire digital financial institution licenses, they’ve additionally launched a spread of coverage measures (ex-post) to deal with the underlying dangers.

9 Within the US, Sq. Monetary Providers and Nelnet Financial institution – two latest ILC constitution approvals – are required to take care of minimal leverage capital ratios of 20% and 12%, respectively, a lot increased than the 8% leverage ratio for different newly licensed banks. Singapore requires digital full service banks to take care of the identical risk-based capital ratios as a home systemically necessary financial institution after an preliminary phase-in interval.

10 This provision may also help authorities to extricate the actions of the financial institution from the tech guardian, if wanted.

[ad_2]

Source link

{kind=link}