[ad_1]

Probably the most vital issues within the monetary independence area is the idea of the 4% Protected Withdrawal Price, or the 4% rule, or just, “The SWR”. This idea basically kicked off the FIRE motion when sure folks realized they may simply withdraw a specific amount per yr from a portfolio of diversified shares/bonds and never go broke.

The 4% rule has loads of controversy surrounding it with supporters and detractors all abound. Nonetheless, it’s a sound funding technique that many individuals (together with myself) swear by. With the intention to perceive monetary dependence, a agency standing of what the SWR is (and isn’t) is totally crucial.

I’ll go into element on this put up of what the 4% rule is, what its limitations are, and if it truly is the holy grail of private finance!

Be aware that the Trinity examine and the 4% SWR was carried out on US market historical past (funding within the S&P 500) the principals apply to different nations as properly.

What’s the 4% protected withdrawal charge?

Should you’re new to the idea of monetary independence and retiring early (FIRE motion), ensure that to learn my put up about how I achieved monetary independence at 34.

Protected Withdrawal Price: The Most charge at which you’ll withdraw out of your funding portfolio with out working out of cash

How do you establish your protected withdrawal charge?

That is the million greenback query (no pun meant). Figuring how a lot cash you want per yr while you retire is crucial step. However how have you learnt how a lot you want?

Relying on who you ask, the solutions will fluctuate wildly.

The Monetary Independence noob

A newby to the FIRE motion would possibly say you want $5m or $50m simply because they by no means considered this query earlier than. My favourite instance of that is once I requested one among my colleagues from one among my earlier jobs what her “quantity” could be.

She promptly replied that she would wish $50m to cease working now. I used to be fully dumbfounded as I knew precisely what she did, how a lot cash she made, and what sort of development trajectory she was on.

Working within the monetary providers business meant above common revenue however in no world would she ever make $50m in her total lifetime. I requested her how she may choose such a quantity when she had no prospects to make such an quantity, thereby by no means with the ability to retire. She simply responded that it could be a quantity she was comfy with. I even requested her if she was planning to turn out to be the CEO to which she mentioned no likelihood.

Some folks simply don’t know what they’re speaking about!

The Monetary advisor

A monetary advisor would possibly inform you that you must have a look at your pre-retirement spending and funds accordingly for that which is able to land someplace between $2m to $5m. They’ll warn you that $1m is just not sufficient as of late since you simply want more cash for no matter. The issue is monetary advisors don’t perceive the early retirement motion and would somewhat not encourage it because it runs counter-intuitive to their enterprise mannequin.

Usually instances, they counsel you want much more cash than you really want so to maintain you working longer and thereby paying their charges for longer.

Your mates who spend means an excessive amount of

A reputable supply could also be asking the chums in your social circle how a lot they suppose they want. No I’m simply joking as that is typically instances a horrible option to go.

I labored my entire life within the monetary providers business and it wasn’t unusual for younger folks to earn a half million {dollars} a yr. On common, folks would earn a minimum of $150k-$200k which could look like some huge cash, however this doesn’t go far in New York. Lots of my pals additionally had no grasp on private finance and would spend cash sooner than it got here in.

Due to this fact, the amount of cash they wanted was excess of the common individual, myself included. A few of them couldn’t even fathom the thought of retiring early as a result of they have been in no place to although they made $200k a yr. As a result of the one life they knew was one among extra spending, their “quantity” was far larger. I imply should you suppose you want want a minimum of $200k a yr in spend, then you definitely’ll want a minimal of $5m to retire.

Fortunately, that’s not the life I ever lived or cared to emulate. Touring the world and residing the great life locations like Bali or Cape City does not require a lot cash in the long run.

The Monetary independence fanatic

The traditional method from the FIRE group is such that you must take your yearly spend and a number of it by 25, thereby arriving on the coveted 4% withdrawal charge. Should you plan to spend $40k a yr, then you must have $40k x 25 = $1,000,000 in your funding portfolio.

Ultimately, $1m is your retirement quantity and 4% is your withdrawal charge, which I believe is a really cheap quantity.

$40k may be your pre retirement spending quantity or it is probably not. $40k may be what your yearly spend will likely be after you retire since you plan to do change your total life and shifting

You possibly can’t predict the longer term, and shouldn’t strive

You by no means know what the longer term holds but when the previous is any indicators, you could be sure you may be taken for the experience of all rides from an financial perspective. Bear markets, monetary crises, and every little thing in between usually are not an if, however when. Nonetheless, it’s a must to choose a quantity on the finish of the day as a result of residing in a world the place you might be planning for the apocalypse is simply not a life that’s price residing.

I made a decision that $40k a yr is greater than sufficient as I all the time knew I would depart the US which is among the most costly locations on the planet. FIRE’ing whereas touring and residing overseas is just not solely cheaper however way more thrilling.

Why does the 4% really work? Cue the Trinity Research

So that you’re asking why does the 4% really work? How did somebody give you this quantity and why does it have a lot acceptance within the FIRE group?

Within the easiest kind, you may consider it as having a portfolio of diversified shares (and or bonds) in your portfolio that pays dividends and appreciates at a median charge of 8-9% per yr earlier than adjusting for inflation. Let’s say inflation is 3% on common over the previous century or so, which leaves you with 5-6% charge of appreciation in actual {dollars}. Should you’re spending 4% a yr, then you’ll all the time have a surplus of 1-2% on the finish of the yr which suggests you must have the ability to dwell off this portfolio without end.

If a historic portfolio can survive a number of wars, recessions, hyper inflation & extra, then maybe it could possibly survive the following 30-50 years

-Trinity Research fundamentals

What’s the Trinity Research?

The “Trinity Research” is a paper and evaluation of this subject entitled “Retirement Spending: Selecting a Sustainable Withdrawal Price,” by Philip L. Cooley, Carl M. Hubbard, and Daniel T. Walz, three professors at Trinity College.

This examine is a backtesting simulation that makes use of historic information to see if a retirement plan (i.e. a withdrawal charge) would have survived beneath previous financial situations.

Put merely, the professors have been asking, “If we had retired at any level over the last century, how a lot may I spend over the length of 30 years with out working out of cash”.

What have been their conclusions?

With a portfolio of a minimum of 50% shares (diversified ETFs like VTI) and the remainder in bonds, you may safely spend 4% of your preliminary portfolio worth adjusted for inflation and have a excessive diploma of confidence that your portfolio will survive 30 years, and sure for much longer.

This examine was first run within the late 90s however has since been up to date formally by its authors to incorporate the monetary disaster and the identical conclusions maintain.

This examine is in fact not meant to foretell the longer term as a result of nobody is aware of what the following 50 years holds. Nonetheless, if we will simulate historic situations which embrace issues like world struggle, hyper inflation, monetary crises, recessions, and every little thing in between, maybe that is considerably dependable for planning for the longer term.

Personally, I believe we dwell in a interval of accelerated change. Issues have all the time modified and advanced all through the ages however as a result of development of know-how, the speed of change for the following 50 years will likely be a lot better than the earlier 50 years. What which means for monetary markets, financial stability, and the Trinity examine is anybody’s guess nonetheless!

How profitable is the Trinity examine?

So is the trinity examine really legit? Except for the precise simulations run by the creator of the Trinity examine, there have been numerous research and simulations run by folks all around the web (thank goodness).

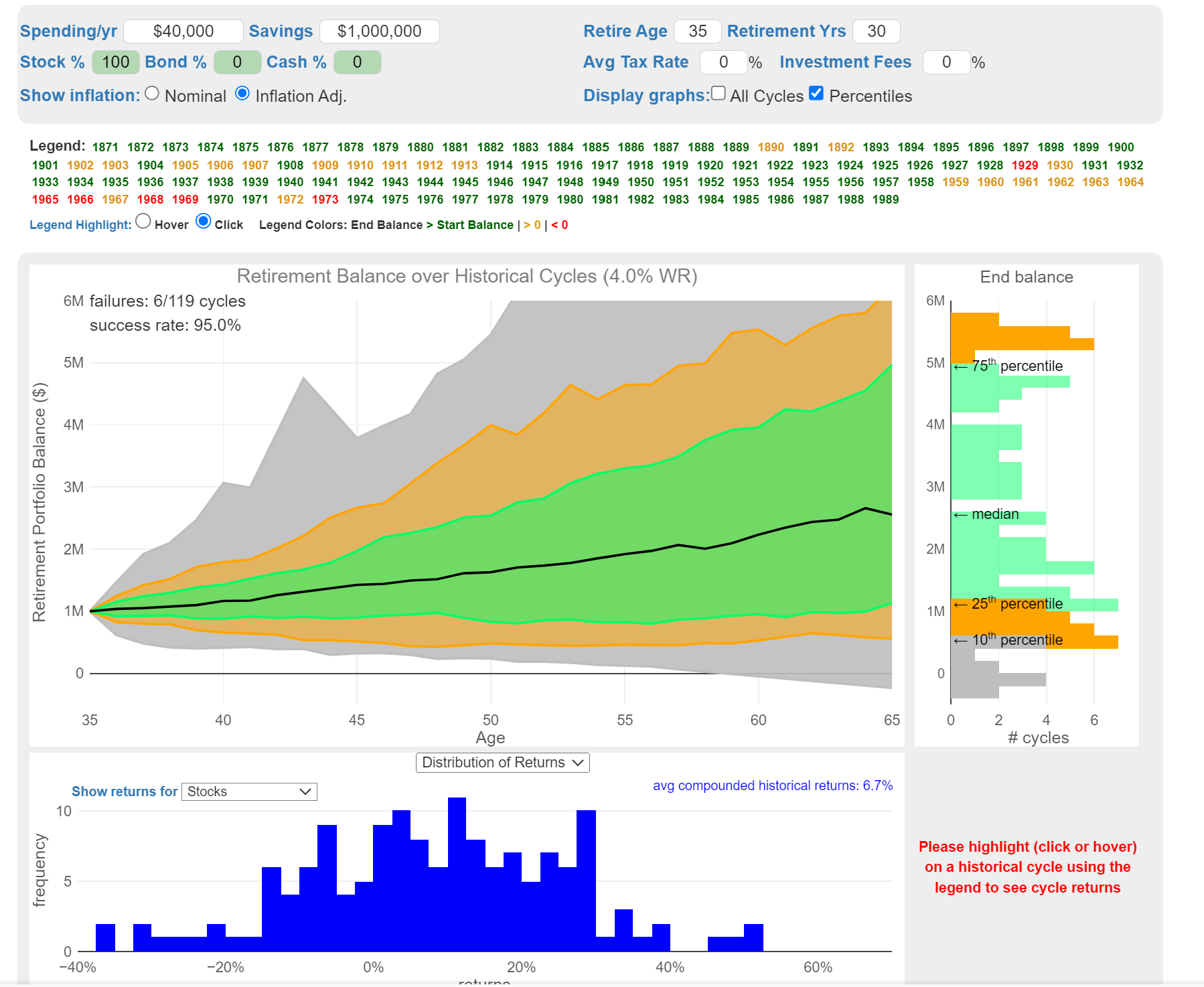

I’ve used the calculator at Participating Information to simulate quite a few eventualities relying on withdrawal charges, the length of your retirement, and the allocation of the portfolio. The calculator then simulates a hypothetical retirement based mostly in the marketplace returns all through historical past. The calculator has historic market information from 1871 to 2019. It’s utilizing actual world historic information to see how a lot cash you’ll leftover. For instance, when you’ve got a 30y retirement horizon, you’ll have retired in 1989 and the calculator makes use of the historic returns from 1989 to 2019 to compute its outcomes.

I ran the under calculator 100 instances or so with completely different variables. As from this screenshot, you may see that this particular run is assuming a 4% withdrawal on a 30y retirement on a portfolio of 100% shares which emulates my private portfolio. I selected the outcomes to be inflation adjusted as a result of that is vital, a median tax charge of 0% as a result of I don’t plan to pay any taxes because of beneficiant long run capital features tax charges, and 0% funding charges as a result of no brokers cost for buying and selling anymore.

As you may see, a 4% withdrawal charge implies that a portfolio of $1m in 1989 would imply I might have a $2.5m portfolio worth on the finish of the 30y interval which implies that it’s greater than doubtless I might have greater than sufficient cash to outlive retirement. The “success charge” is 95% which suggests the 4% protected withdrawal charge could be very strong.

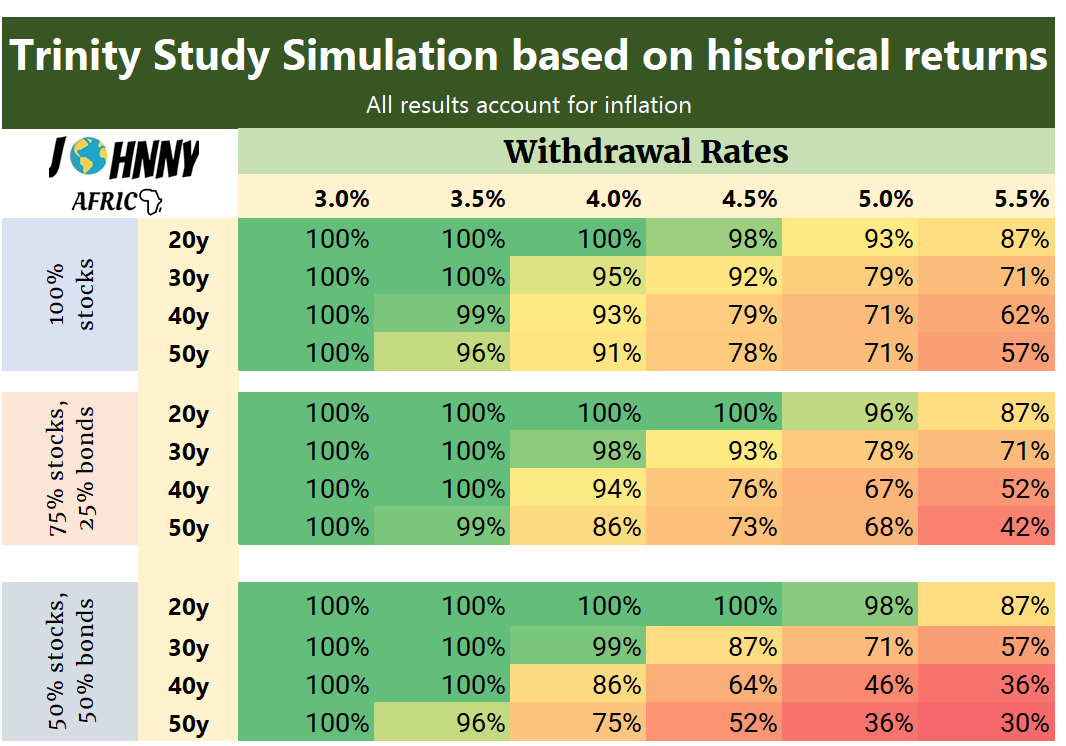

The under desk is working this calculator with varied withdraw charges and retirement durations. Somebody like me will most undoubtedly require greater than 30 years in retirement. I’m 35 in spite of everything. With common dwell expectations rising as a result of medical developments, somebody like me ought to be planning for a 50-60y retirement (hopefully).

As you may see, the 4% withdraw charge could be very efficient assuming a portfolio of principally diversified shares. With a portfolio of 100% shares, I’ve a 91% likelihood of constructing it by a 50y retirement. I didn’t embrace something over 50 years into this desk as a result of the outcomes for a 60y, 70, 80y retirement have been fairly much like 50 years.

A decrease withdraw charge of three.5% basically meant you all the time succeeded in accordance with the Trinity rule.

The next allocation to bonds was usually much less profitable than larger fairness portfolios doubtless as a result of bonds have drastically underperformed in latest instances. Whereas usually, the frequent thought course of is extra bonds as you grow old to attenuate volatility however I’m unsure it is a prudent transfer because it was prior to now.

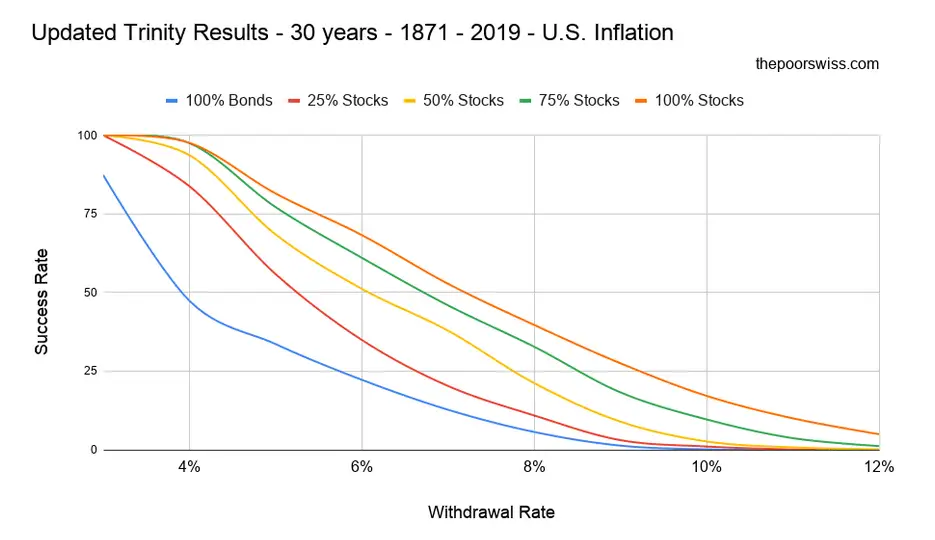

The Poor Swiss has a really good chart summarizing the above based mostly on completely different withdrawal charges and portfolio allocations.

What withdrawal charges work?

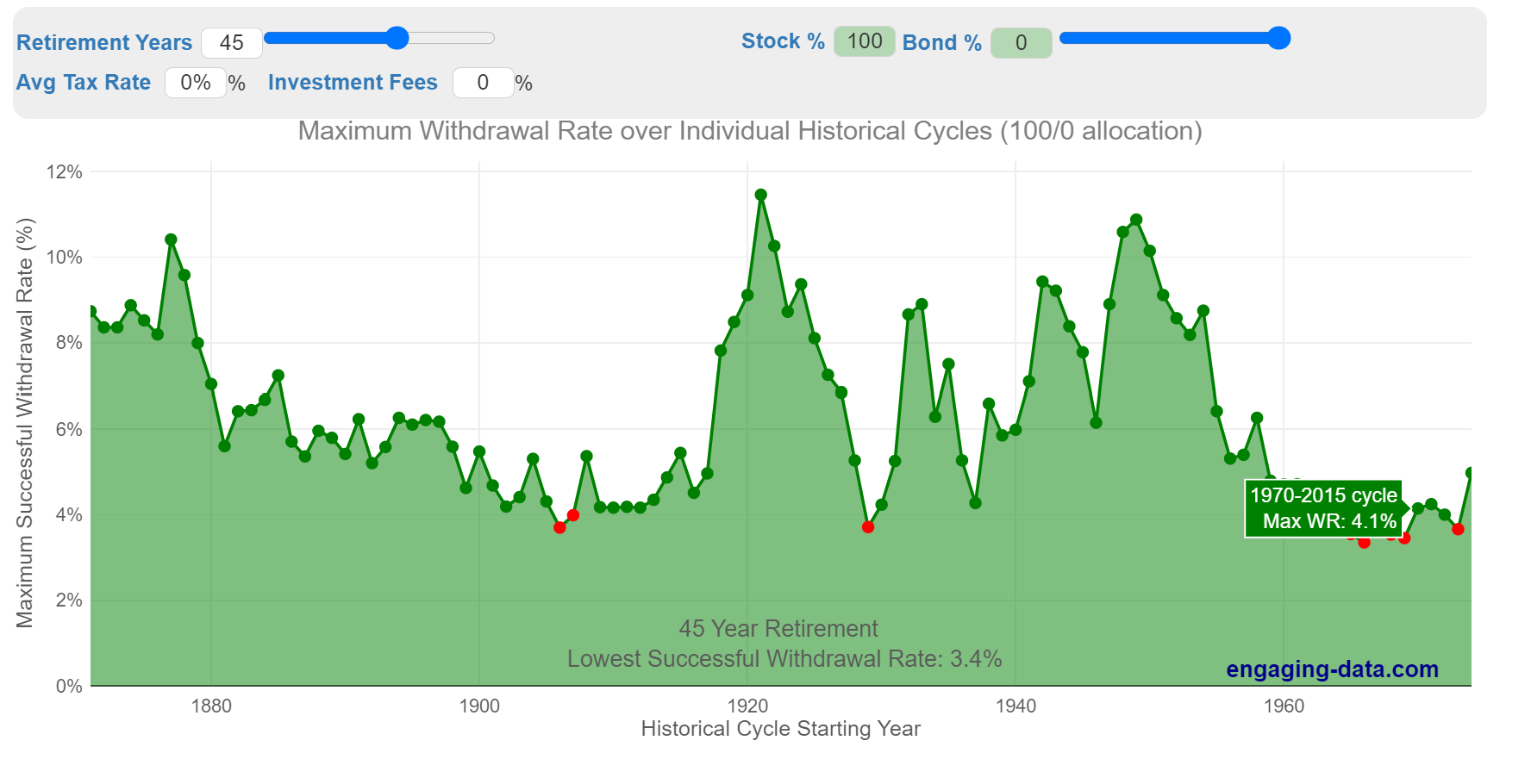

To additional stress the Trinity examine, Engaged Information has one other calculator that permit’s you play with what SWR would have labored relying on the yr you retired.

I selected an instance with a forty five yr retirement and a 100% allocation to shares as I plan to principally be in shares all through my life. As you may see, the 4% withdraw charge has been virtually all the time profitable.

Should you had a forty five yr retirement beginning within the late Sixties, you’ll have ended within the early 2010s which might have meant you went by the Tech bust of the 2000s and the good recession. Due to this fact, a withdraw charge of three.4% would have been required to outlive that situation.

Does the SWR account for inflation?

Shares in idea outperform different investments when inflation rises. This won’t be the case to start with when inflation first begins growing as a result of worry within the markets, however over the long term, shares carry out properly. It is because if a giant company will increase costs whereas total salaries enhance, then total income ought to subsequently enhance resulting in a bigger share value.

The frequent observe for utilizing the SWR is to extend your yearly withdrawal by the inflation quantity. For instance, if the CPI (inflation) is 5% in a yr and your protected withdrawal quantity is $40k, the following yr you may withdraw $40k + $2k = $42k and your portfolio will likely be in tact.

In actuality, your actual inflation figures will likely be completely different than the official CPI report launched by the Authorities. Quite a lot of these numbers are impacted by housing and vitality prices which could indirectly have an effect on you as it would others. Conversely, you would possibly see that you simply want more cash than what the CPI is since you spend more cash on meals and going out for instance.

Adjusting your SWR by inflation is merely a suggestion, a means of claiming that the examine works and accounts for the inflation.

Retiring proper earlier than an enormous market crash

Should you occurred to retire in 2000 on the top of the Tech bubble, you’ll have seen a direct crash within the worth of your portfolio to the tune of 35%. The portfolio recovered over time however then you definitely have been hit with the Nice recession which worn out 50% of the worth of shares. It wasn’t till 2011 that the losses from 2008 have been recovered.

Sequence of Returns Threat

On this case, you’ll have had a misplaced decade and your returns would have been muted. Withdrawing out of your portfolio when the market is on the lows will severely affect how a lot cash you’ve gotten sooner or later. In different phrases, while you retire is definitely essential.

That is known as the sequencing of return danger, aka the chance of retiring within the fallacious sequence of occasions. You need to most ideally time your retirement (While you cease working) to not coincide with market highs as a result of you’ve gotten a better likelihood of markets dropping and taking your retirement portfolio with you.

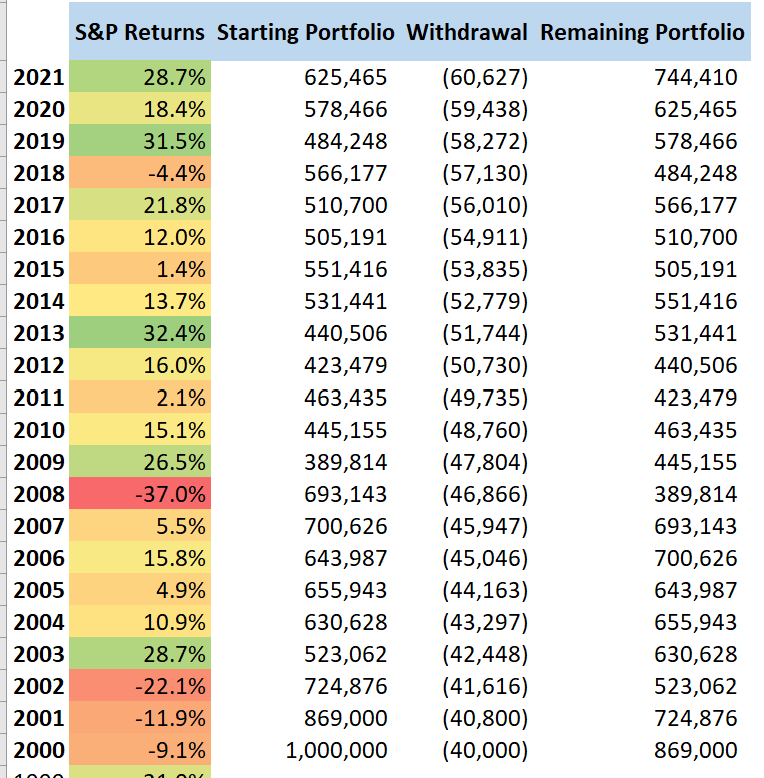

Retiring in 2000

Here’s a desk that exhibits the historic returns on the S&P 500 on a beginning portfolio of $1m, and a 4% withdrawal charge that will increase by inflation yearly (assumed 2%).

As you may see, the early 2000s weren’t type to traders. Should you had $1m invested in 2000, it could be price simply over half of that 3 years later assuming a $40k yearly withdrawal. Due to how a lot you misplaced from the start, the portfolio by no means actually recovers even 20+ years later!

Keep in mind: The Trinity examine is not a flat 4% withdrawal yearly relying in your portfolio steadiness however merely 4% of your beginning retirement steadiness.

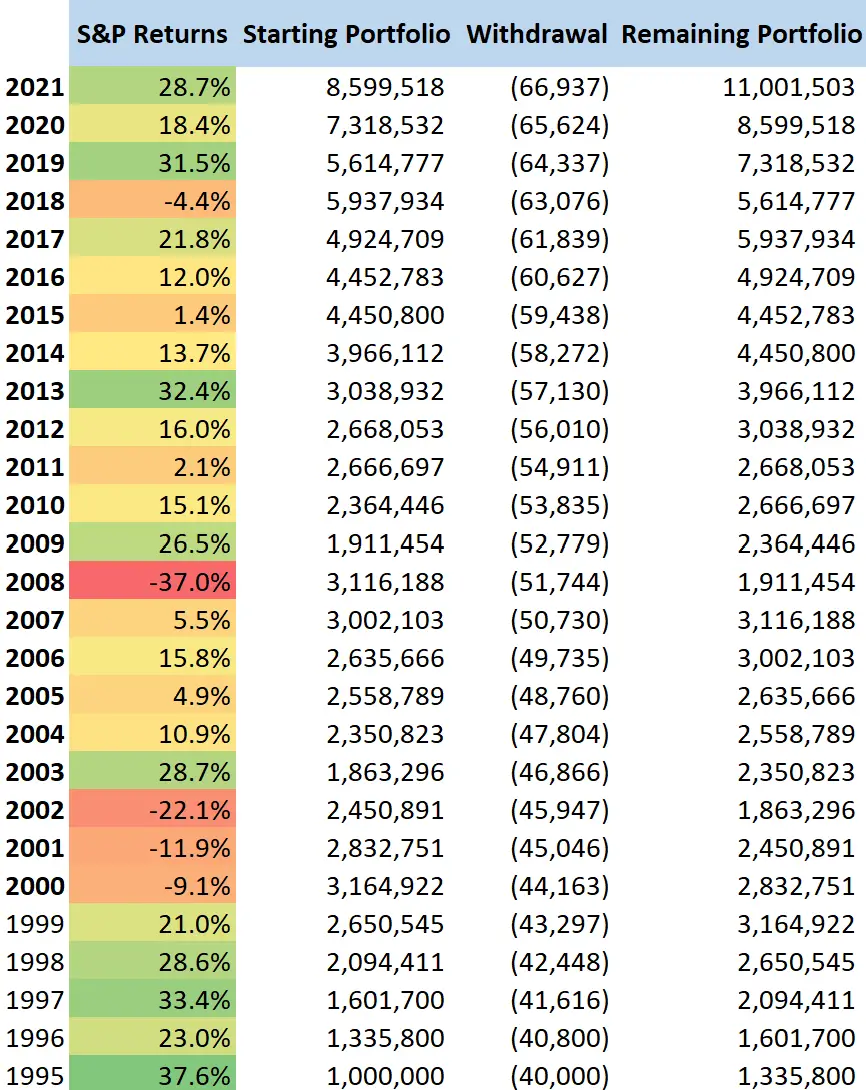

Retiring in 1995, completely completely different

Should you retired 5 years earlier with $1m within the financial institution, you’ll have had a a lot completely different situation. The mid 90s have been very sturdy for the markets and you’ll have virtually doubled your cash earlier than getting into the tech bust.

As you may see, this image is extraordinarily completely different. Sure you’ll have nonetheless misplaced some huge cash through the tech bust and the Nice Recession as you may see from the declines in 2002 and 2008. Nonetheless, as a result of the worth of your portfolio is already so excessive, withdrawing $40k to $50k is a considerably smaller share of your total portfolio than the sequence of danger returns from the primary instance.

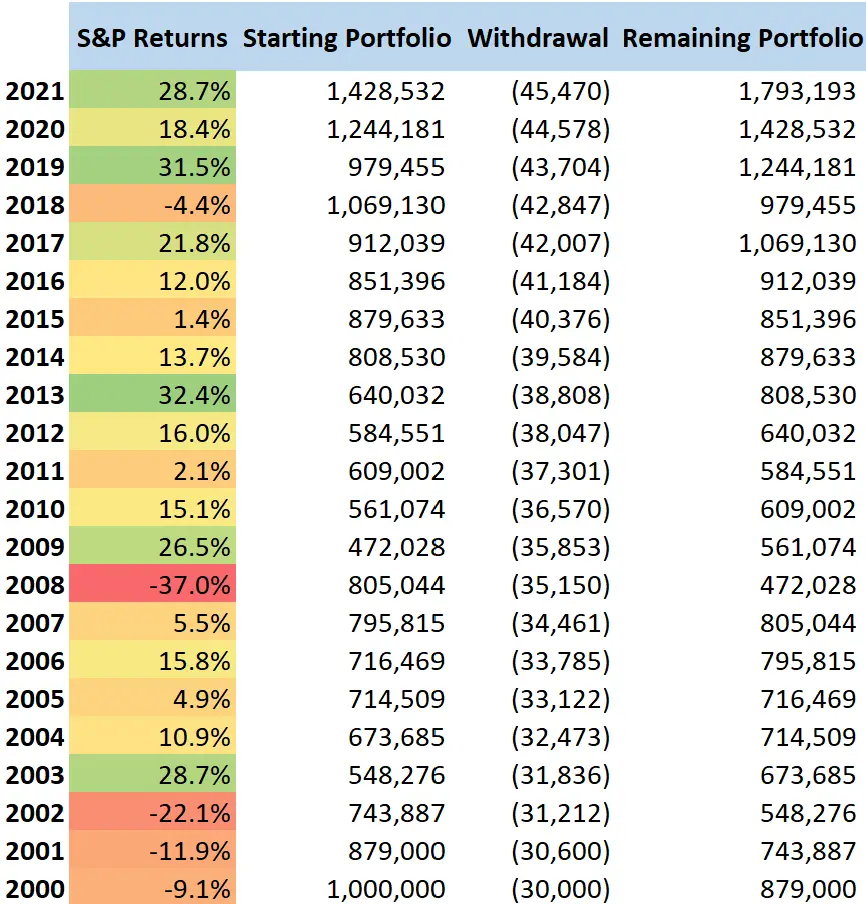

Retiring in 2000 however with a 3% withdrawal charge

Should you retired in 2000 with a 4% withdrawal charge, it could have been scary to look at your portfolio crumble. Nonetheless, should you switched this to a 3% withdrawal charge, you may see how shortly this adjustments the equation.

Merely lowering your spending will drastically enhance your possibilities of success (which was already confirmed within the desk from the part above). As you may see, if I modified to a 3% withdrawal charge, then I might have virtually $2m in my portfolio as of 2021. It is a enormous distinction vs retiring in 1995 but it surely nonetheless beats the unique situation!

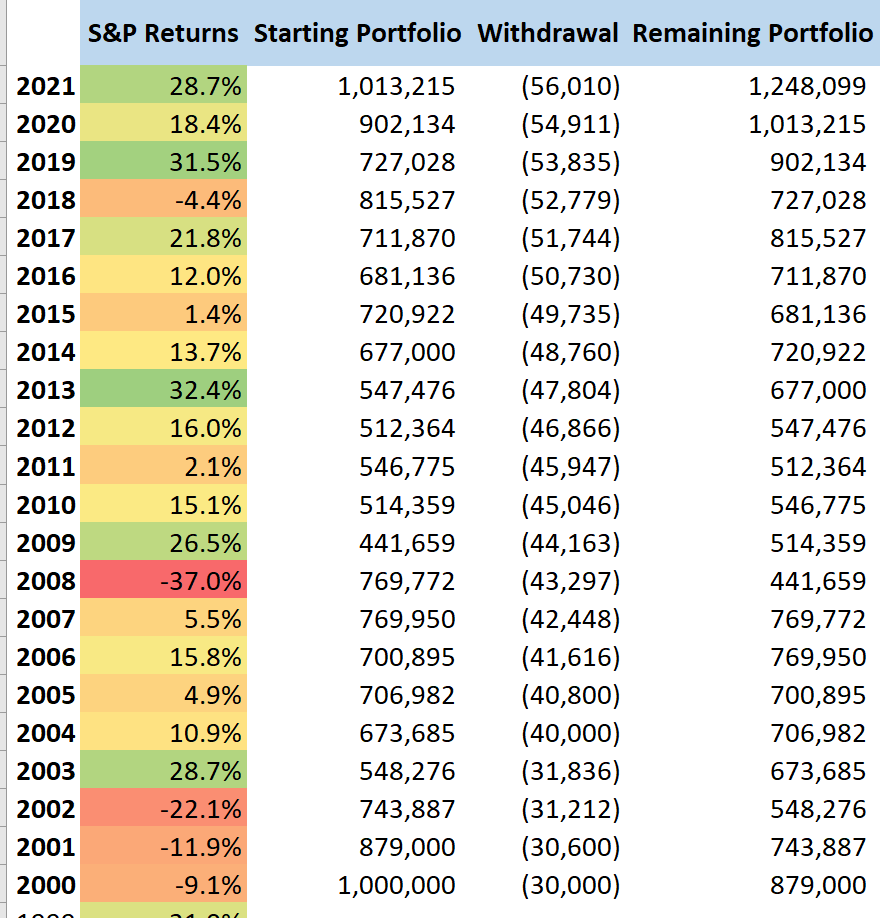

After all, this defeats the aim of a 4% withdrawal charge so let’s see what it could appear to be if I began with a 3% withdrawal charge in 2000, and switched to a 4% withdrawal charge in 2003 as soon as I noticed the market was bettering.

You find yourself with a smaller portfolio as you’d count on however you might be nonetheless above your preliminary funding.

Find out how to decrease the sequence of returns danger?

Ultimately, it’s not possible to foretell what’s going to occur with markets. You may be one of many very unfortunate few that pulls the set off proper earlier than a bear market. This might sound scary however in the long run, it’s a must to pull the set off in some unspecified time in the future, in any other case you’ll simply by no means find yourself doing it out of worry.

There’s no idiot proof option to decrease the sequence of returns danger however listed below are a number of the methods I make use of.

- Make use of a bond tent: Allocate extra to bonds to start with years however swap to equities after the primary few years.

- Construct in a ample cushion: As a substitute of retiring proper while you hit your “quantity, take into account working a number of extra months to pad your portfolio

- Decrease your withdrawals throughout bear markets: It’s unlikely it’s essential to spend precisely 4% a yr. If there’s a protracted bear market, decrease your withdrawal charge to three% and wait it out.

- Withdrawing solely on the market highs: I solely withdraw when the markets at or are close to their highs. I’ve ample aspect revenue to cowl my daily bills in addition to different actions like promoting choices to generate passive revenue.

- Facet or half time revenue: In protracted bear markets, there’s no disgrace in looking for an additional supply of revenue whether or not that’s going again to work or doing a aspect hustle.

Is a 90% SWR success charge ok?

As you may see from all of the above analyses, the 4% SWR is definitely considerably of a really conservative situation. Sure there are situations the place the 4% fail however generally, it’s fairly a strong calculation.

In lots of the examples, even withdrawing 5% a yr yielded unfounded success with portfolio worth rising considerably.

Trinity examine is extra than simply 30 years

The Trinity examine was completed on a 30y time-frame. For early retirees, it’s doubtless you’ll want much more than 30 years. 50-60 years is the extra sufficient time-frame particularly as medical advances imply we are going to all dwell longer.

However as you’ve seen within the earlier examples, the SWR is sort of strong for retirement durations longer than 30 years, for much longer in actual fact.

In abstract, the 4% withdrawal charge will get you properly previous a 90% success charge. Success is outlined as not working out cash, or having an account worth above 0 when the retirement interval is over.

However is it actually this simple? Can you actually sleep sound at night time simply setting any such recommendation on autopilot?

Listed below are some frequent complaints in regards to the Trinity rule and listed below are my feedback

- The time interval the Trinity examine was performed in was in a time of prosperity and development; this received’t be the case sooner or later

- Sure, the examine was performed throughout instances of development. Nonetheless, this development was additionally met with a number of wars, recessions, hyper inflation, a number of monetary crashes and extra. Not saying that instances sooner or later received’t be completely different in fact, however who can predict this?

- Inflation will outpace any features and wipe out my portfolio. Prices like healthcare, housing, meals and so forth. have all outpaced CPI

- Prices for healthcare and housing have undoubtedly outpaced the inflation charge, that is definitely. Nonetheless, the return of the S&P takes this under consideration and with rising prices, markets will rise as properly. That’s what the Trinity examine relies off of. Worst case, simply transfer out of the US to a rustic with first world healthcare 🙂

- The 4% withdrawal charge has failure and also you run the chance of nonetheless going broke

- This isn’t unfaithful, however will you reside your life based mostly on one thing that has a really small likelihood of occurring? If that’s the case, when will you ever really retire since you’ll all the time be fearful of working out of cash?

Trinity examine doesn’t account for any further revenue made throughout retirement

The Trinity examine relies on the truth that you’ll by no means work or earn one other greenback once more or change their retirement methods just like the under:

- By no means earn one other dime, whether or not it’s by aspect revenue like running a blog or taking over some half time job

- No further revenue from social safety or recurring pensions

- By no means adjusting your withdrawal charges: That is vital as a result of as talked about above, I might completely decrease my spending if markets have been to materially decline

- By no means spend much less as you age (which is frequent)

The 4% protected withdrawal charge is merely a examine that makes use of mounted assumptions. It truly is extra of a suggestion, a common overview of tips on how to FIRE for dummies. In observe, it’s unlikely you’ll spend precisely the 4% withdrawal charge yearly, and it’s unlikely that you simply’ll be a dull robotic following the instructions of some monetary paper.

Should you’re financially savvy sufficient to acquire a portfolio of $1m+, it’s doubtless you factored in a big cushion, although the 4% rule says you don’t want one. It’s additionally doubtless that in a interval of monetary stress, additionally, you will regulate your way of life accordingly to plan for the worst.

When does the Trinity examine not work?

Listed below are the situations the place the Trinity examine is now not legitimate and actually there’s just one.

You materially change your retirement plan

Maybe you resolve to have kids which in fact will drastically enhance your spending.

Possibly you resolve that you simply need to be a baller and need to purchase fancy automobiles. Absolutely a $40k withdrawal charge won’t be sufficient.

Otherwise you need to begin a brand new enterprise and require some preliminary capital outlay. If it is a important endeavor, then you definitely aren’t actually retired anymore?

The 4% Withdrawal charge is sweet sufficient

So whereas there’ll all the time be detractors for the 4% rule, I believe it’s really fairly reliable. Ultimately, this examine and technique is only a guideline. Your actual world state of affairs will all the time differ and also you’re human which means you’ll regulate with the instances. Nobody is aware of how a lot healthcare will price sooner or later, however nobody can predict what sort of technological revolutions come together with it.

The world will change and you’ll change with it too.

Personally, I infrequently withdraw 4% as a result of I do know I could make up for withdrawals with my passive revenue from running a blog in addition to buying and selling. After all, we will’t neglect about all my bank card journey hacking which permits me to fly at no cost.

Within the years since attaining FIRE, I’ve traveled the world solely to see my internet price enhance and I’ve solely actually withdrawn one thing like 1.5% or 2%. The 4% rule is there for me to grasp that within the worse case the place I select to do completely nothing, my portfolio will likely be sufficient to resist the take a look at of time.

The 4% rule is right here to remain and I can suggest so that you can use this calculation as properly!

Proceed Studying:

[ad_2]

Source link

:max_bytes(150000):strip_icc()/Health-GettyImages-1477523726-d9489f5e044241b097588b0636bf7561.jpg "Solar Poisoning: Indicators and Signs")

{kind=link}